Stablecoins are moving what we call Crypto more towards just “this is just Digital Money now.”

This two-part article series examines the current landscape of various “stablecoins” to clarify labels that often sound functionally descriptive but frequently aren’t. It also highlights under-discussed aspects in this evolving space. We need clearer understanding of what these assets are and as importantly, what they’re not. Even with the GENIUS Act and ongoing work on the CLARITY Act, significant ambiguity remains for some token types.

Stablecoins are not one thing. They’re a family of tokens with dollar-like claims, and the important questions aren’t whether they appear stable, but what kind of claim they represent, what backs them, who gets the yield, how they redeem, and what happens under stress.

Along the way, I’ll go into some of the oddities and implications of stablecoins. Some may seem slightly off topic. However, they’re all part of what’s becoming this ecosystem and therefore I believe useful in understanding how things fit together.

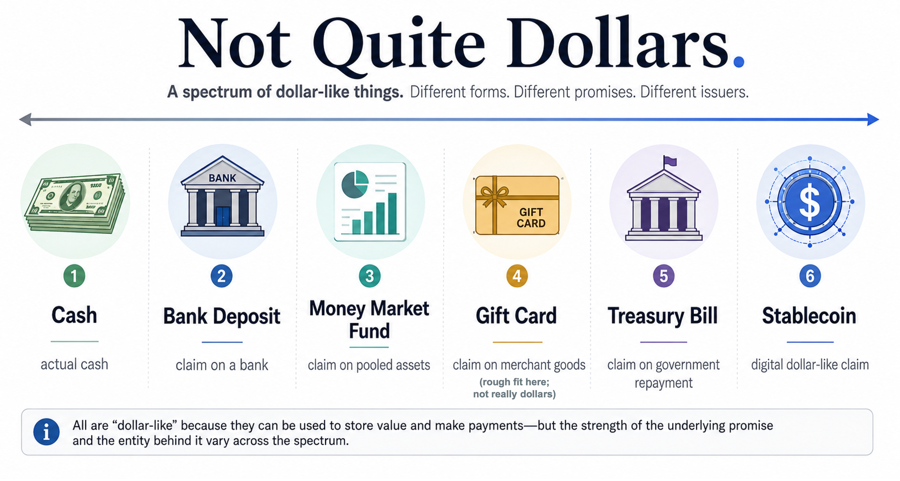

There are a lot of definitions for stablecoins and I’ll give you a basic one in a moment as well. But the point here is there’s a variety of flavors, often appearing stablecoin-like, but aren’t exactly. Sometimes a variant seems stablecoin-like because it is in some ways, but has differences that arguably should call into question just how stable it might be. Let’s try coffee as a metaphor. Drip coffee, espresso, cold brew, and lattes are all coffee drinks. An energy drink with coffee flavoring, however, is trying to be in the category. Maybe kind of is, but it’s really fundamentally something else. Now back to dollars. Cash in your wallet, a bank deposit, a money market fund, a prepaid gift card, and a Treasury bill can all be thought of as “dollar things.” However, some are actually dollars, while others could be thought of more as close cousins.

Anyway, the typical high-level definition of a stablecoin is something like this: Stablecoins are digital assets intended to maintain stable value by pegging them to traditional assets. Typically this is a currency. And most typically, the U.S. dollar.

Meanwhile, some things referred to as stable are legitimately stablecoin-adjacent, while others are only borrowing the label. This doesn’t necessarily mean some are false or bad. Just that they may have different behaviors and values and it could be important to understand them in terms of what your goals are and what risks might be.

Stablecoins & New Things

We often struggle with labels for new things. When people name new things they often try to offer context with familiar labels. Though we can stumble on terms that seem adjacent, but don’t match cleanly with what things actually are. (Horseless carriage for cars, the “wireless” for radio, electric candle for light, and so on.) This makes sense, because the way we come to understand new things is usually through the old. It’s called apperceptive learning. The challenge is when we attach meaning to new things they may come with ideas that don’t really apply exactly.

Then there’s the reality that most of us don’t use advanced financial instruments for most of our daily needs. Though sometimes, we might fall into such a need. My wife and I have a conversation about oil futures every year. Why? Our heating oil company lets us lock in contract pricing or use floating pricing options so all of a sudden we need to make choices like oil commodity experts? Stablecoin tools and markets are likely to affect everyone soon enough, whether working with them directly or not. So it’s probably a good idea to at least go over the basics beyond “they’re just pegged to a dollar.”

The Stablecoin Sort of Peg

As mentioned, a stablecoin is a digital token designed to hold a stable value relative to something supposedly stable itself, like a national currency. Most often, at least for now, that’s the U.S. dollar. So one USDC or one USDT is intended to be worth one dollar. The key word is “intended.” It doesn’t mean the token is a dollar. It means there is some structure, promise, reserve, market mechanism, or redemption process that’s supposed to keep it behaving like one. These stablecoins are not government issued. They’re issued by private firms and backed by reserve assets. (Or they’re supposed to be anyway.) They are not magic internet dollars. They’re claims, instruments, or mechanisms designed to act dollar-ish in digital environments. And the details of their workings matter a lot.

Why Stablecoins Matter

Stablecoins matter because they may be one of the first crypto things that makes sense even if you don’t care about crypto. I’d even argue they’re not even “crypto” so much anymore. They’re just digital assets that use blockchain technology.

Early stablecoin thoughts were about avoiding volatility in crypto trading. Kind of like a safe parking spot for funds. But the real action and value right now for stablecoins is commercial and institutional. Faster and less expensive payment rails, cross-border, settlements, and more. All are drivers for mass adoption. We’re talking market sizes with current estimates of $300 billion or more. There’s other growing use cases such as micropayments and AI agent payments, however, it’s traditional finance adopting these rails faster than anything else.

This doesn’t mean they’re risk-free or they’re all the same. It just means they’re useful in ways a lot of earlier crypto assets weren’t. They become the cash-like leg of digital asset markets, payments, trading, settlement, remittances, DeFi, and increasingly, tokenized real-world assets (RWA).

Analogies for the Basics

Gift cards may be a somewhat useful analogy for understanding stablecoins, as long as we don’t push it too far. But let me try pushing this idea a bit anyway and then wrap it up with how they’re different, because compare and contrast is sometimes enlightening.

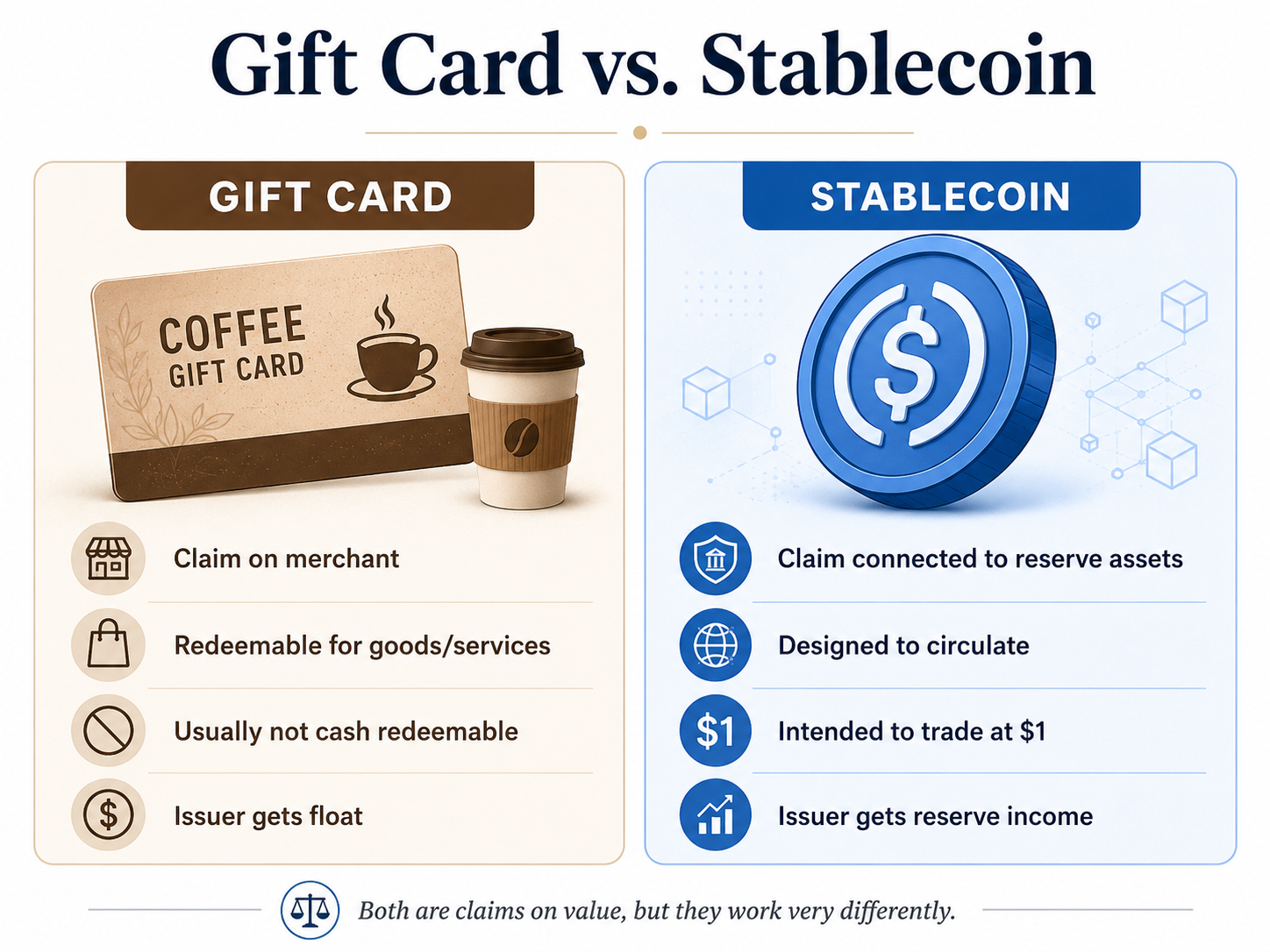

Neither stablecoins nor gift cards are the dollars themselves. Both are a claim on value issued by someone else. Let’s use a Starbucks gift card as an example. You give $100 cash to Starbucks and get a $100 Starbucks card. Now Starbucks has your $100 and you have a claim worth $100 at Starbucks. Starbucks can invest or use the money while you burn down your card over a week or two, (or sooner depending on your caffeine or scone needs). Alternatively, you got the card as a gift, but you don’t drink coffee much and the card sits in your junk drawer for a year. Or you maybe even lose it. Starbucks earns the float on that $100, but of course, owes you in product to the value of your balance. So the gift card is not money. Its balance is a liability of Starbucks. (In this case, non-cash.) Next, we’ll move on to a real stablecoin now, such as USDC. The name makes it sound like a government thing, but it’s not. It’s issued by a private company. You give $100 to Circle and get 100 USDC. Or more likely a downstream on-ramp company and they source the USDC from somewhere, but eventually it came from Circle. (Never mind how, that’s a topic for another article. See: How Does Fiat Become Cryptocurrency) Circle has reserve assets and you have a claim represented by USDC. Circle earns income from reserve assets and keeps most of the yield. Again, USDC is not the underlying dollars. It’s a claim on a liability issued by Circle. (I said “most” of the yield because sometimes Circle may share some with partners like Coinbase and others. And this is arguably one of the more important business models in stablecoins.)

Okay, some are probably jumping ahead and already understand where this analogy breaks. And this is the instructive part. A Starbucks gift card is redeemable only at Starbucks. It’s not intended to circulate broadly and usually cannot be redeemed for cash. Whereas USDC is designed to circulate, is transferable globally, intended to trade at $1 and is redeemable through the issuer. (Again, maybe not directly, but via an exchange or other off-ramp.) That’s a huge difference. Yes, there are some types of stored value things that travel, such as credit card points spending on partner goods or services, airline miles maybe gifted away, and so on. But they still usually live inside a controlled network, account system, or redemption program. They are not generally fungible, globally transferable bearer instruments intended to trade at par with dollars across open markets.

The Really Interesting Comparison

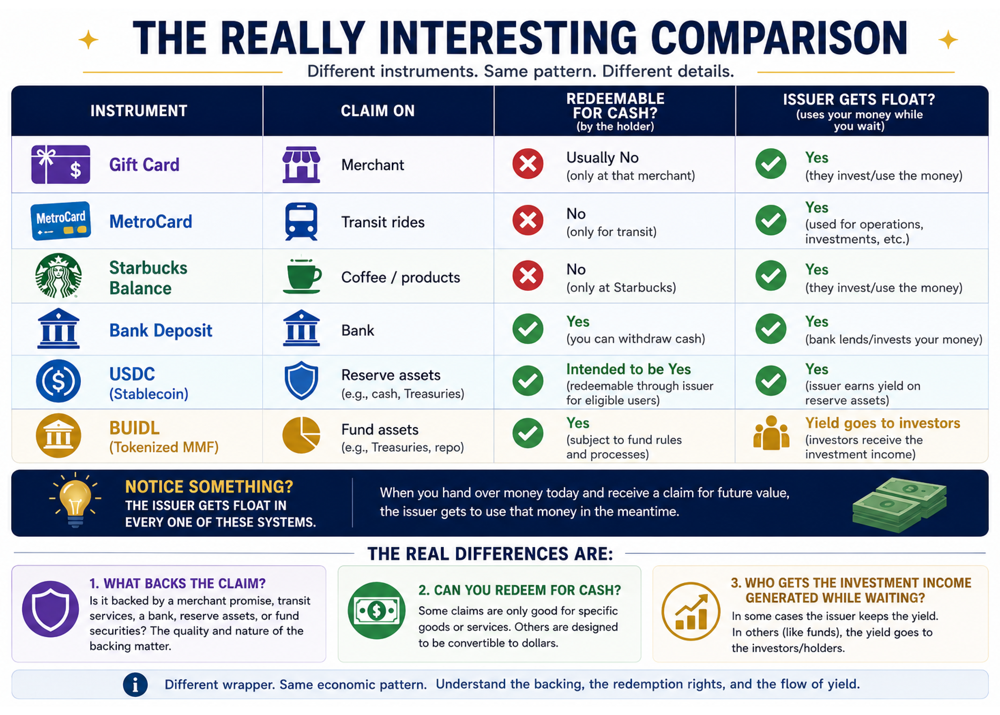

If you line these things up, some patterns get easier to see. A gift card is a claim on a merchant. A MetroCard is a claim on transit rides. A Starbucks balance is a claim on coffee or products. A bank deposit is a claim on a bank. USDC is a claim connected to reserve assets. BUIDL is a tokenized claim on fund assets. They are not the same thing.

What are the differences? When we compare, we should be asking… What backs the claim? Can you redeem it for cash? Who gets the float or investment income while the claim is sitting out there? Where the heck did I leave that Amazon Gift Card?

That part about the float benefits is the one people often miss. In many of these systems, the issuer receives cash up front, gives you some kind of claim, and then benefits from the use of that cash while waiting to fulfill the obligation later. Sometimes that obligation is coffee. Sometimes it’s a subway ride. Sometimes it’s dollars. Sometimes it’s a fund redemption. It all has a stored-value flavor. But very different legal and economic realities. What most of them have in common is you’re most often not earning anything off this capital. However low big bank interest rates may be, it’s not nothing. And there are credit unions, online banks, and some fintech accounts with somewhat higher rates, though the insurance details depend on whether the account is FDIC-insured, NCUA-insured, or held through a partner bank. Maybe this is ok if you’re using stablecoins as a safe space when doing transfers. Or to save a lot on international remittances. But if you’re holding it longer term for stored value? Stable is really a misnomer. Stable only means stable against the dollar in nominal terms. It does not mean stable purchasing power. If you hold a non-yielding stablecoin long term, inflation can still quietly reduce what that dollar claim is worth in the real world.

Where This Leaves Us

So a stablecoin is not simply a digital dollar. It’s a dollar-like claim. Sometimes that claim is designed for payment. Sometimes it looks more like stored value. Sometimes it starts to look like a fund, a savings product, or something else entirely. And even when all of these things are denominated in dollars, or meant to stay close to a dollar, they may not be the same thing underneath.

Once you start asking those questions, the stablecoin label gets a lot less simple and that’s where things get more interesting. If stablecoins are a family of dollar-like claims, then the next question is what kinds of claims are we actually talking about?

This is where Part 2 will pick up.