In Part 1, we discussed the many dollar-like claims of stablecoins. That matters because once we stop treating “stablecoin” as one single thing, the more important questions come into focus. What kind of claim is it? Who issued it? What backs it? Can it be redeemed? Does it pay yield? Who gets the float, and more.

So Part 1 was about the mental model: stablecoins as dollar-like claims. Now it’s time to go over why those claims are not all stable in the same way.

Legal Stablecoins vs. Stablecoin-Like Things

This will vary by jurisdiction, of course. But in the U.S. context, the important phrase is not just “stablecoin.” It’s “payment stablecoin.”

A payment stablecoin is supposed to be a digital asset used for payment or settlement, designed to maintain a stable value relative to money. It’s not supposed to be a bank deposit, money market fund, security, or interest-bearing investment product. It’s meant to be more like a digital payment instrument backed by safe, liquid reserves.

USDC and USDT are the obvious examples people usually mean when they say stablecoin. They’re the early most popular dollar-pegged tokens intended to trade at or near $1 and function as payment, trading, and settlement instruments. Though it seems many are justifiably envious of these business models and want their own stablecoin. Who wouldn’t? What a great business. Though how many there can be is likely a highly constrained thing. How much liquidity is the whole world willing to lock up after all? This is probably a “winner-take-most” type of market.

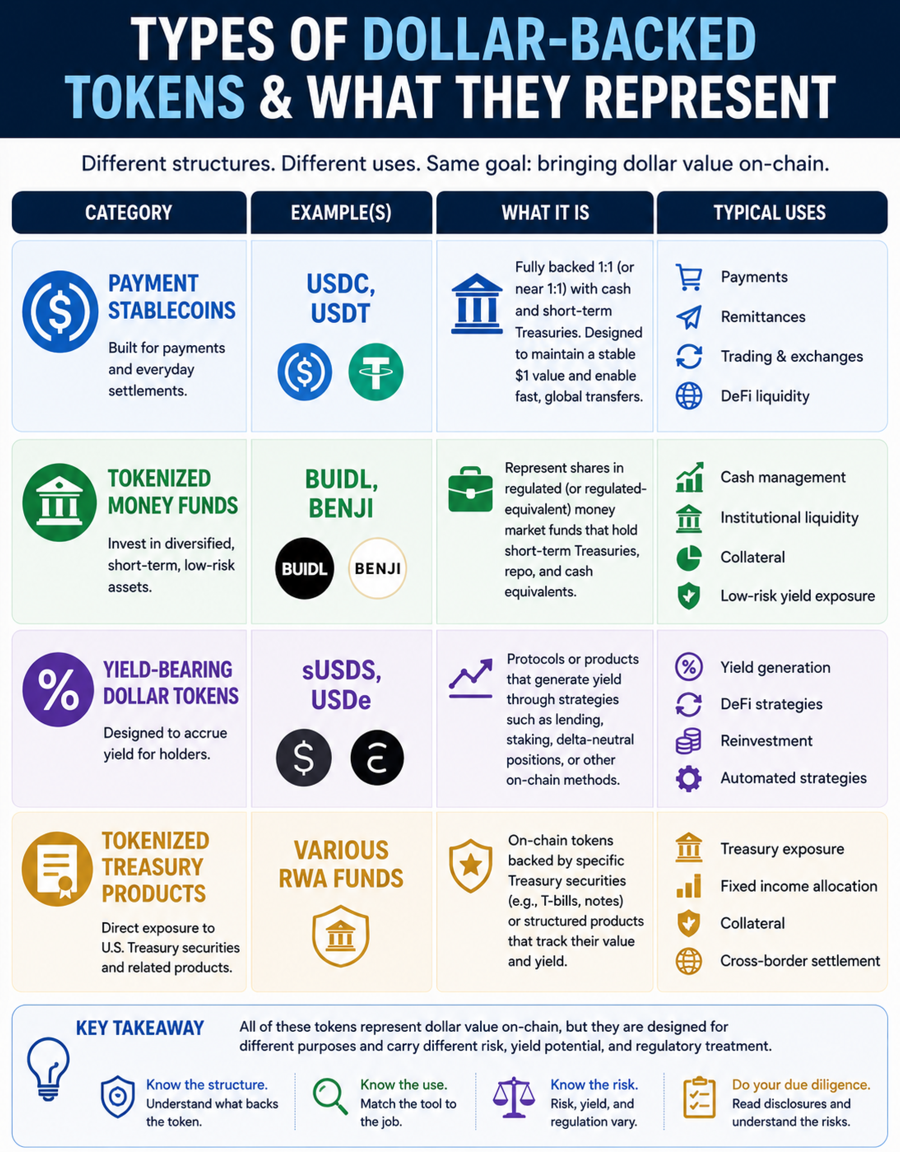

Besides the tokens closest to the payment-stablecoin model, there are other tokens that sound or feel similar. sUSDS sounds dollar-ish. USDe sounds dollar-ish. Tokenized Treasury funds feel cash-ish. BUIDL and BENJI may move in stable dollar-like ways. Some of these may be useful. Some may be well-designed. But legally and economically, they may not be the same thing. Once a dollar-denominated token starts paying yield, it starts looking less like a stablecoin and more like an investment product.

A yield-bearing dollar token is not the same as a payment stablecoin. Tokenized money markets or synthetics built around derivatives? Nope. Also not the same as a reserve-backed stablecoin.

This is also why trading them at “1:1” can be misleading. Lindy Han gets into this nicely in “Zero-Fee Stablecoin Swaps Don’t Exist. Stop Saying They Do. Two things can both look like dollars and still have different risks, different cashflows, and different economics.

So for the rest of this discussion, when I use the word stablecoin, I’m really talking about payment stablecoins unless noted otherwise. Because “stable” may describe the intended or claimed price behavior. A branded token name that kind of sounds stable-ish though? That doesn’t by itself tell you what the thing is.

Not Everything That Looks Like a Stablecoin Is One

Sometimes things are legitimately slightly different, but kind of have the same vibe. Other times, people are maybe abusing the privilege of trying to hook on to a meme. The largest challenges here are likely when things are very similar, but actually have subtle differences that are important. Not every attempt to be a dollar look-alike is the the same.

Payment stablecoins like USDC and USDT are generally meant to function as digital dollars for payments, trading, and settlement. Tokenized money funds like BUIDL and BENJI are more like fund shares that happen to live on-chain. Yield-bearing dollar tokens like sUSDS or sUSDe may aim to stay dollar-like, but they’re also designed around generating yield. USDe itself is better described as a synthetic dollar, while sUSDe is the yield-accruing version. Tokenized Treasury products may be dollar-denominated and relatively stable, but they’re really exposure to Treasury-like assets.

These things can all be valued at or very close to a dollar and feel cash-like. But they are not necessarily the same product category. And this is where our current language gets slippery. Calling all of them “stablecoins” is convenient, but it can hide the real differences in redemption rights, reserves, regulation, liquidity, yield, and risk. This will vary by jurisdiction of course. I’ll stay with U.S. law, but it does seem as if the world in general is starting to coalesce around some definitions and guidelines.

Some of the different types:

Why The Distinction Matters

The distinction matters because “stable” can sound like a promise about safety. But it’s more about intended price behavior. Two tokens can trade around $1 and have different working mechanisms. One might be backed by cash and short-term Treasuries. Another might represent a fund share. To a casual user, they may all look like dollar tokens. But to a regulator, risk manager, or anyone trying not to lose money, those differences are the whole point. Stable is not the same as safe or insured or easily redeemable.

We should have maybe called them mostly stable-ish. Okay, that might not be fair. If well designed, these are useful tools of value. It’s just that all of a sudden, finance has gone from being kind of like what cable television used to be vs. the complexities of managing all your own media now. A lot of what used to be under the hood finance normal people didn’t care much about is now sometimes leaking into both business and consumer concerns. We need to all pay attention.

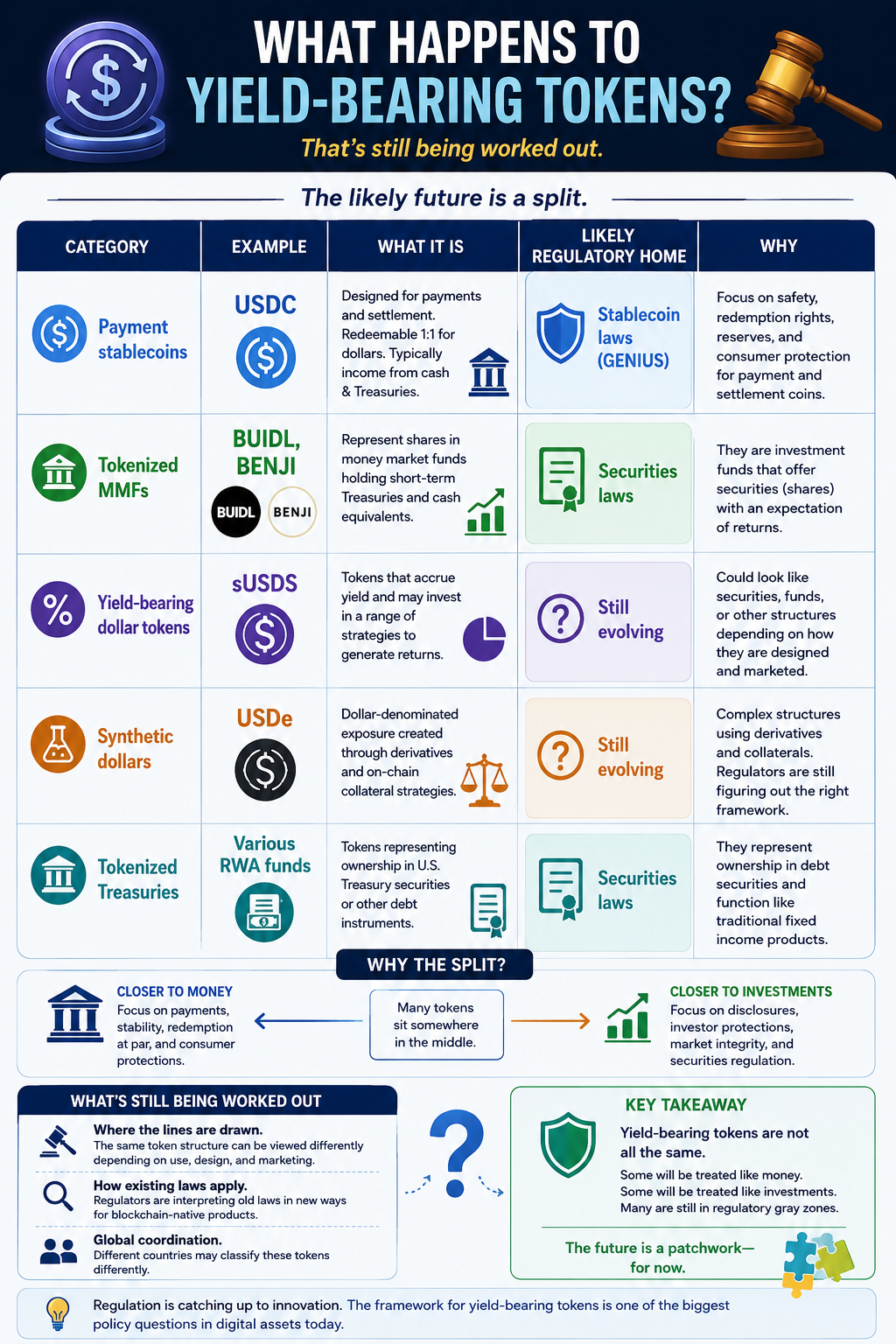

How things are regulated is another issue. Things were being regulated through enforcement actions instead of a clear statutory framework. Are these things securities or commodities or something else? So the GENIUS Act is mostly related to payment stablecoins, which puts it in banking-adjacent payment-infrastructure territory. Whereas things like yield-bearing tokens? Some, like tokenized treasuries might be securities and others commodities. Others are still unclear and evolving, even with the GENIUS Act and ongoing CLARITY Act / market-structure efforts. So this is where to take care, “stablecoin” seems to be becoming an umbrella marketing term that covers several economically different things.

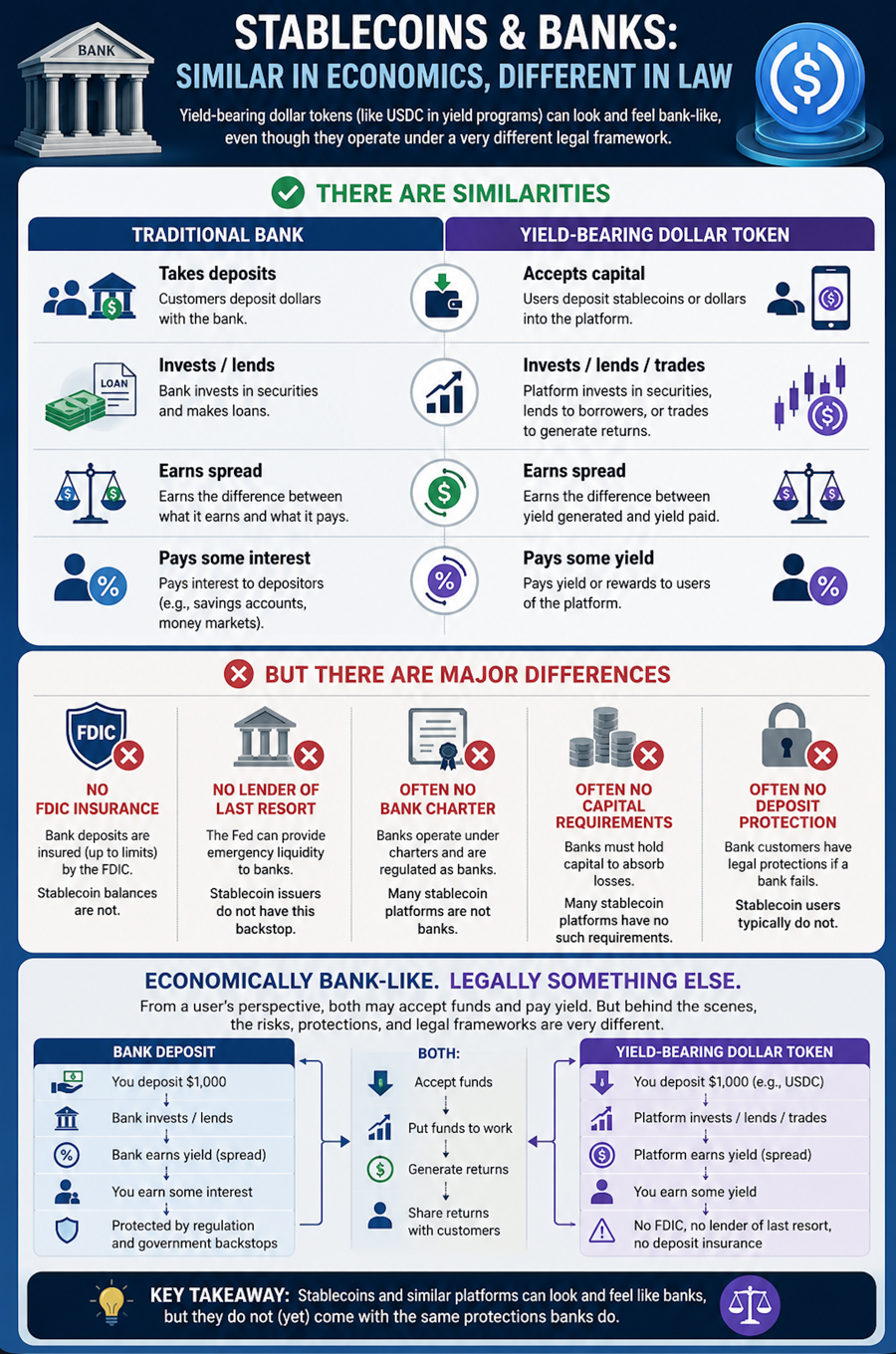

You might be wondering, “Hold on, if stablecoin issuers can’t pay interest, how can holders get yield from them? I see people offering yield!” Here’s the trick. USDC, for example, does not pay interest. But this doesn’t mean someone else can’t pay you interest for letting them use your USDC. Consider old-fashioned cash. A dollar bill in your wallet earns nothing. Put that dollar in a bank savings account and the bank may pay you interest. The dollar itself didn’t change, but the rules around it did. It’s the same with USDC. Coinbase can offer a separate rewards program funded through its own economics or other arrangements, while the USDC token itself remains non-interest-bearing. However, the stablecoin issuer itself, (like Circle), is not paying interest. If it did, it would be acting more like a bank deposit or similar. Is this really splitting hairs? Perhaps. But this is how the laws are shaping up.

So… it seems stablecoin issuers are being asked to act like narrow banks in some ways, while prohibited from acting like full banks in others. Is this just generally good or done to protect the entire banking system from an implosion? Banks pushed back hard on yield loopholes out of fear that higher yield stablecoins would suck deposits out of traditional banks and destroy their lending capacity. Basically, policymakers worry about what happens if stablecoin issuers become bank competitors.

Crazy? Maybe. Confusing? Perhaps a bit. Economically, issuers getting treasury yield and maybe sharing some with a business partner, then an exchange offering some yield products seem rather similar. But legally they’re just not. The separation of what issuers can do vs. others may be artificial. But regulators care about who is promising the yield, what assets back the promise, whether deposits are insured, and who bears the risk if things go wrong. Those legal distinctions are what separate a payment stablecoin from a bank deposit, even when the user experience starts to converge.

What Happens to Yield?

This is one of the weirdest and most important parts. (To me anyway.)

With a plain payment stablecoin like USDC, the holder generally doesn’t receive interest just for holding the token. The issuer holds reserve assets, those assets may earn income, and the issuer keeps that income, sometimes sharing parts of the economics with partners. That’s the business model. And it’s absolutely brilliant.

But once a dollar token starts paying yield directly to the holder, we’re in different kind of place. Maybe the yield comes from Treasury bills. Maybe it comes from lending. Maybe it comes from a DeFi protocol. Maybe it comes from a derivatives basis trade. Maybe it comes from some promotional subsidy. The point is that the yield has to come from somewhere. And once the yield comes from somewhere, there is usually some extra risk somewhere. Remember, these things being held can’t be risky. They’re the “Real” dollars that your token represents. Really, stablecoins are closer to transferable IOUs than literal dollars. And that goes back to some of the regulatory issues. What kind of risk can be taken where and where’s the potential damage. What it comes down to is avoiding the blast radius taking out entire financial systems. We’ve seen that movie, right?

There’s another wrinkle here regarding yield risk here. Some of these yield opportunities may look small and boring, which can make them feel safer than they are. A few percent APY sounds almost bank-like. But if the yield comes from an on-chain lending vault, DeFi protocol, bridge, liquidation system, or smart contract, then the risk profile is not bank-like at all.

That does not mean every vault is reckless or every protocol is doomed. Some are carefully designed, audited, curated, and monitored. But the basic math still matters. If the upside is a few percent a year and the downside is a meaningful chance of permanent loss, then the product should not be mentally filed next to a savings account just because the asset inside it is USDC.

This is another reason the label matters. Holding a payment stablecoin is one thing. Putting that stablecoin into a yield strategy is another. The dollar-like token may be stable. The strategy around it may not be.

There’s also what I’d call a speed-to-patch problem. If AI tools make it easier to find smart-contract bugs, attackers may be able to search for weaknesses faster than protocols can safely patch them. Some contracts are intentionally hard or impossible to change. Others are upgradeable, but upgrades may require governance, multisig approvals, timelocks, audits, or emergency procedures. Pausing a protocol may stop damage, but it does not magically fix the underlying problem. So even if the asset inside the vault is a stablecoin, the wrapper around it may depend on software that is hard to repair quickly under attack. See what Aram Mughalyan says about “The math in DeFi is completely broken”. This is supposed to be a benefit of – at least somewhat – immutable contracts. But also potentially a major vulnerability. I think what we’re going to see with more future DeFi products is interesting combinations of public/private, somewhat permissioned chains to try to balance things like risk, privacy and transparency. Meanwhile, just be aware of these issues as factors to consider.

Is an Earning Stablecoin Rehypothecation?

Not really. But it does represent a risk layer. When I’d originally learned about stablecoin holders being offered yield, I’d learned more about rehypothecation around the same time. And I thought, “Hey, that’s rehypothecation!” As it turns out, no.

Yield does not automatically imply rehypothecation. However… Even if something isn’t rehypothecation, it can still involve maturity risk, counterparty risk, liquidity risk, and run risk because the money is no longer literally sitting in a vault.

Let’s look at what rehypothecation is.

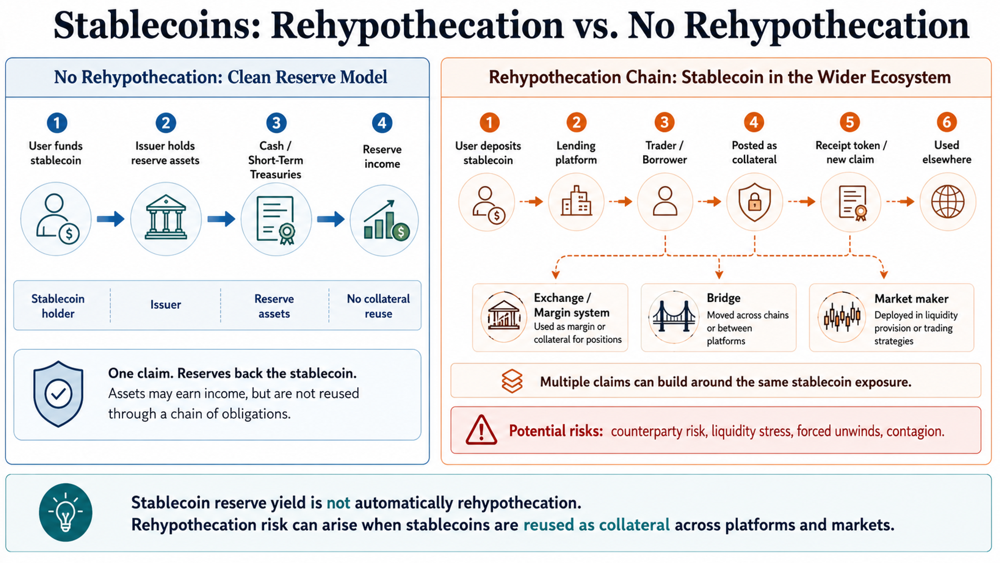

Rehypothecation occurs when an asset that has been pledged or deposited is reused by an intermediary for another purpose. For example:

- You deposit securities with Broker A.

- Broker A uses those securities as collateral for its own borrowing.

- The same underlying asset is now supporting multiple obligations.

The asset has effectively been reused.

Now consider this scenario of yield without rehypothecation. Let’s say Circle holds $1 billion of customer funds invested in short-term Treasury bills. Treasuries pay interest and that interest flows to Circle. (Well done Circle.) No rehypothecation occurred because the same dollar isn’t supporting multiple claims. The reserves simply earned interest. There is only one economic claim being represented. The token is just a digital claim intended to be redeemable for a dollar, backed by reserve assets. That reserve dollar itself is not being lent out ten different ways. And this is essentially how USDC operates today. (Among others; this was just one example.)

So is rehypothecation with stablecoins a non-issue?

Not quite.

In the clean payment-stablecoin model, reserve yield itself is not rehypothecation. If an issuer holds cash and short-term Treasuries, and those assets simply earn income, that may be a very nice business for the issuer, but it does not mean the same underlying asset is being pledged and reused through a chain of obligations.

Waitaminute, didn’t I just get finished saying how stablecoins earning yield from reserves at issuers was a great business and not rehypothecation? Yes. But… wait, there’s more.

Stablecoins do not only sit at the issuer. They move into exchanges, lending platforms, DeFi protocols, margin systems, bridges, tokenized asset markets, and market-maker balance sheets. Once that happens, they can become collateral in a much larger financial machine.

For example, I might deposit USDC into a lending platform. That platform might lend it to a trader. A receipt token or claim against that deposit might then be used somewhere else. A market maker might borrow stablecoins, post them as collateral, hedge against them, and use the same general pool of liquidity across multiple trading venues. At each step, the original stablecoin may still be simple. But the claims around it can multiply. I might responsibly put my tokens into a decent yield-bearing place. Or I might accept the marketing of some too-good-to-be-true 25% yearly rate, which might have risks I don’t really understand. My choice. But this section isn’t just about my personal risk. It’s about systemic risk.

That’s where the risk comes in. If everyone treats stablecoins as cash-equivalent, but those same assets are also being lent, pledged, wrapped, bridged, or used as collateral across multiple systems, then stress in one place can spread quickly to others. A borrower defaults. A bridge fails. A lending market freezes. A token depegs. A market maker pulls liquidity. Suddenly, what looked like “just dollars on-chain” starts looking more like a chain of claims, dependencies, and forced unwinds.

So the scary part is not necessarily that payment stablecoin reserves are rehypothecated by default. The scarier possibility is that stablecoins become the common collateral layer for a sprawling digital financial system, while the claims around them multiply in ways that are hard to see until something breaks.

And we have seen versions of this movie before in traditional finance: a supposedly safe or liquid asset becomes a linchpin across many transactions, then one failure or liquidity shock cascades through everyone who depended on that asset behaving like cash.

Liquidity and Stablecoins

Liquidity is another place where the word “stable” can do too much work. A stablecoin may be intended to be redeemable for $1. But there are at least two different worlds here. One is issuer redemption. The other is secondary-market trading. If you’re an eligible customer, you may be able to redeem directly with the issuer. That’s one thing. If you’re selling through an exchange or swapping through a DeFi pool, you’re relying on market liquidity. That’s another thing. Most ordinary consumers would not redeem USDC directly with Circle. They usually use an exchange, broker, wallet, bank, or other off-ramp.

This is also where the simple story of stablecoin payments starts to hide a lot of machinery. Receiving USDT is one thing. Delivering Brazilian reais, euros, Kenyan shillings, Nigerian naira, or Philippine pesos is another. Somewhere in the background, someone has to manage wallets, custody, blockchain settlement, payment orchestration, FX, local liquidity, KYC, KYB, AML, sanctions checks, banking relationships, payout rails, reconciliation, and reporting.

When all of that works, the user just sees money arrive. But the stability of the token is only one part of the experience. The rest depends on the infrastructure around it.

Most of the time, these line up closely enough that nobody thinks about it. One USDC trades for roughly one dollar. One USDT trades for roughly one dollar. Fine. But under stress, the difference could matter. A token can temporarily trade below $1 even if the issuer still claims redemption will work. That’s not necessarily a permanent failure. It may be panic, liquidity stress, uncertainty, or friction. But for the person holding it in that moment, it feels very real.

So liquidity is part of the stability story.

What’s going to happen as more tokenization starts to occur across multiple markets? One value is supposedly 24/7 trading. Maybe. Then again, when there’s hundreds of exchanges of various types that are live 24/7 for both people and bots, is it possible that actual value will be radically distorted just due to liquidity swings?

We’ll see soon enough how this all shakes out and how stablecoins factor in.

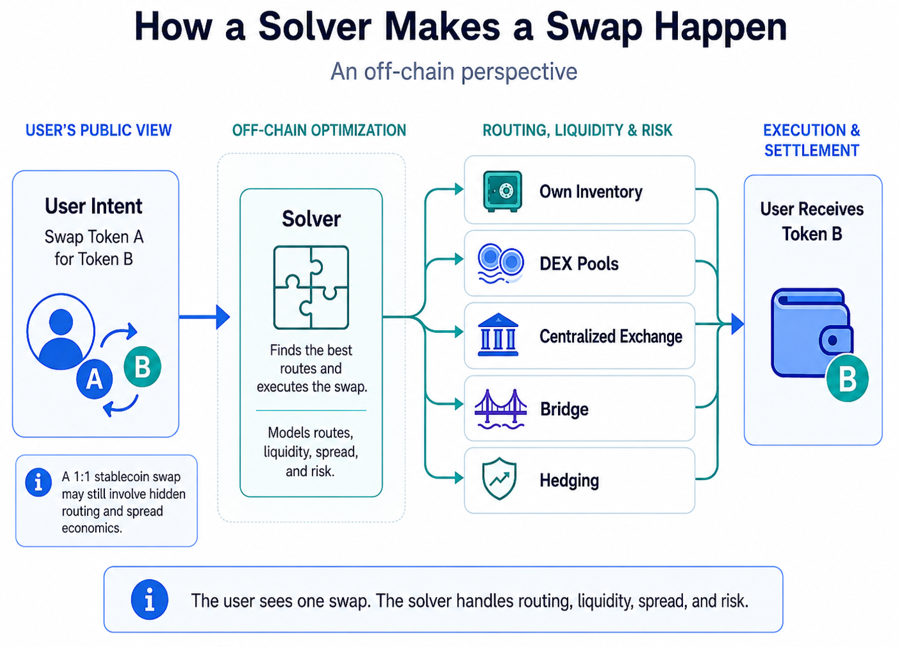

What’s a Solver?

I didn’t really understand what this was when I kept coming across the label. You might, but just in case not, here’s what I’ve learned. This all gets especially interesting when these assets are traded or swapped. If two dollar-like tokens have different reserves, different redemption rights, different yield, or different risk, then “1:1” is not necessarily a neutral market price. Again, see the excellent article by Lindy Han mentioned earlier, “Zero-Fee Stablecoin Swaps Don’t Exist. Stop Saying They Do.” Anyway, this brings us to another weird little word in this world: solvers.

A “solver” is another crypto-ish term. Personally, I had assumed it was just an aspect of a blockchain node that executed as a smart contract, or some autonomous thing living inside the chain. It sounded like it, so that was my assumption. Mostly, no. A solver is usually an off-chain actor, though the final settlement may happen on-chain. Maybe a trading firm, market maker, arbitrage desk, or yes, it could be an automated trading system. They figure out how to complete a user’s intended transaction.

It seems almost like an auction house to me. Let’s say you say: “I want to swap this token for that token, under these conditions.” The solver says: “Okay, I can make that happen.”

Then the solver figures out the route. Maybe it uses its own inventory. Maybe it routes through Curve, Uniswap, a centralized exchange, a bridge, or some combination of all of them. Maybe it hedges the other side. From the user’s perspective, the trade just happens. Behind the scenes, someone solved the execution problem.

This matters for stablecoins because when someone says they can swap USDC for USDT, or USDC for USDe, or USDC for some yield-bearing dollar token at “1:1” with “zero fees,” a solver may be one of the actors making that happen. But the solver still has to deal with spreads, liquidity, inventory risk, hedging, and the fact that two tokens that both look like dollars may not be economically identical.

So “zero fee” may just mean you don’t see the fee. It doesn’t necessarily mean no one is being paid for taking risks of flowing money or tokens around.

As for the term itself, it seems to come more from optimization and computer science than traditional finance. In math and software, a solver solves a routing, matching, constraint, or optimization problem. In DeFi, the trade is framed the same way: the user wants an outcome, and someone else solves for the best way to get there. In traditional finance, we’d probably call some of these actors dealers, market makers, liquidity providers, or arbitrageurs. Crypto calls them solvers because the system treats the trade as a problem to be solved. I’m not sure I’ve been able to find the actual original source of the term. If someone reading this happens to know, please reach out and share that.

What Happens When Things Get Lost

There’s one other difference with stablecoins from other digital assets that I don’t think most people discuss. It’s what happens upon loss.

When I worked in New York City, I always wondered about my old-style metro card. How was the value stored on it being used? And how much got lost? Like gift cards, the stored value entitled you to something. In this case, rides. The city used the float. But if you lost the card, that value was gone. Over time, unredeemed balances become a form of breakage, similar to gift cards. Accounting treatment can get complicated, but economically the transit authority benefits because it collected money for rides that were never taken, whether the cards were lost or just kept as souvenirs. Again, such cards are not like USDC because they’re not redeemable for cash. But they’re similar in that they’re all forms of prepaid claims on a future obligation; just of different sorts. It’s interesting that the city, (or the MTA/transit authority), basically lost most of that revenue when going to contactless smartphone payment. (Though there is still some use of stored value cards.) Maybe they save more on infrastructure of physical card management. Still, an interesting lesson in what happens when float disappears in some transaction flows. Anyway…

Sticking with Starbucks, (or any other retail gift card), let’s see what happens when you lose this card, which is essentially a bearer instrument. Starbucks still has the money. Eventually accounting rules allow the company to recognize some of that unredeemed balance as revenue. This is called breakage. Years ago, at least in the U.S. laws were passed about this because it was seen as unfair to make them expire, however, companies also can’t just keep liabilities on their books forever. Upon loss, customers lose the claim. However, the issuer keeps the economic benefit. This is one reason gift card programs can be quite profitable.

Is it possible to lose stablecoins? Sure. Easily. For starters, there’s the classic crypto problem of using a self-owned wallet to which you lose your private keys. Yes, like bitcoin, the tokens are there, but effectively unusable and gone. Or you may have messed up and sent stablecoins to a burn address or otherwise unrecoverable incorrect address or wrong network. They could get locked in a broken smart contract. And then there’s death Without Recovery Instructions; See Estate Planning & Digital Assets.

There are plenty of stories how bitcoin has been famously lost; we just haven’t heard that much about stablecoins yet. Now, it is true that sometimes it may be possible to recover stablecoins differently than bitcoin losses. Many major stablecoins include administrative controls. For example, issuers can sometimes freeze or block list addresses, reissue tokens and comply with court orders. So there may be recovery options. But my examples are more wonderings about what happens when there’s not.

Stablecoin lost tokens probably remain outstanding. Let’s say 100 USDC are issued, but the private key is lost forever. Nobody can access those tokens. The 100 USDC still exist on-chain and the reserve assets still exist. Circle does not automatically get the money. The tokens simply become inaccessible. However, Circle would continue to benefit from any income from the reserves. No expiry. That is one hell of a business. It’s interesting because lost Bitcoin tends to reduce the effective supply. It may still be onchain, but effectively? Circulating supply is reduced while total minted supply remains the same. Economically, the reserves backing those lost tokens may never be claimed. At some point this starts looking a little like gift-card breakage, however legally and operationally it’s much more complicated because the tokens technically still exist. (Either way, it’s good to be a major issuer, right?)

Wrapping Up

I believe stablecoins are one of the more important developments in digital everything right now, finance and otherwise. It’s not just about payment rails and settlement per se. It’s about maybe finally enabling that elusive dream of micropayments that can perhaps open up a great many business opportunities. And without this type of payment, would AI agents be able to function as well as they otherwise might? Then there’s usage of IoT devices… the list goes on.

So yes, it may be that the stablecoin label is starting to cover too much. Some are payment instruments. Some stablecoin-like things are investment products, tokenized funds, synthetic dollars, yield products and more. Some are trying to be cash-like. Some are trying to be dollar-like while doing something much more complicated in the background.

That’s why the question shouldn’t just be, “Is this a stable thing? It says it is!” We really need to ask how and why something is stable. What’s it really backed by. And maybe most importantly, can it handle real stress. It’s a great label, but we absolutely need to understand what the reality of it means when we work with these assets.