This is about understanding risks in tokenized finance. The fact that is, the Wrapper is not the Thing. As U.S. regulators, courts, and market participants continue working through the legal treatment of tokenized assets, it’s perhaps worth stepping back from the hype and asking a simpler question. What are these instruments actually giving us and what is their actual nature?

Noise around Real World Assets, or RWAs, can be confusing. I think part of the problem is the overuse of the word “tokenization.” And there’s still a mental connection to the idea of “crypto” as a wild landscape of speculative games, even though today’s tokenization is maturing into both more traditional as well as new creative opportunities. There are complexities with tokenization, but at a high level, is this really so different from what finance has been doing for centuries? Think about it. Have we ever lived in a world of pure ownership when it comes to financial assets? For a few things in your possession, maybe. But for most financial assets, ownership has long been mediated through contracts, records, custodians, issuers, and legal claims of some sort.

Before blockchains, stablecoins, prediction markets, or tokenized assets, much of economic life already depended on representative ownership. A deed represents a claim to a house. A stock certificate represents partial ownership in a corporation. A bank balance represents a claim against a bank, not a stack of specific dollar bills sitting in your name. A warehouse receipt can represent goods in storage. And so on.

Modern finance is built on layers of representation. We just maybe don’t often think about it all that deeply because we’re just used to it.

The difference now is we’re extending this representational logic much further. We’re not just representing ownership of assets. We’re representing exposure to prices, outcomes, events, benchmarks, reserves, indexes, collateral pools, and more. Sure, we’ve had some of this. But now it’s extending into everything, or seemingly so. That’s the deeper pattern behind prediction markets, tokenized real-world assets, stablecoins, synthetic assets, and oracle-driven crypto finance. They may have different purposes and risks, however, they’re also similar. Finance has always traded claims. What feels different now is the ease, speed, programmability, and apparent simplicity with which more kinds of reality can be turned into tradable exposure with fewer traditional intermediaries, and in forms that may look deceptively simple to investors.

These things are not necessarily ownership of reality. Or even always actual ownership of the underlying asset. Often, they’re just exposure. And this bears a little thought.

For example, a contract can be based on oil without the trader ever touching a barrel of oil. A token can track the price of a stock without giving the holder shareholder rights. A stablecoin can trade like a dollar without being the same thing as a bank deposit. A prediction market contract can pay out based on an election, court decision, inflation print, or sports result without the buyer owning anything except a conditional claim. Each of these things has different mechanisms and increasingly more clarity of legal status. And each of these things has a different purpose, from real producers of real goods trying to decrease their risk, to speculative bettors.

I think this raises a strange but increasingly important question:

Is everything going to be a derivative?

From Ownership to Exposure

The core idea behind a derivative is simple: its value is derived from something else; whether the price of wheat, the S&P 500, Treasury rates, Bitcoin, or even the outcome of an election.

In traditional finance, derivatives are often used for hedging. Airlines hedge against rising jet fuel costs, while farmers lock in crop prices to protect against declines. In both cases, the goal is not generally to win a trade, but make the future more predictable by shifting unwanted risk to someone willing to take it.

Every trade needs a counterparty who could be an opposing business risk, a speculator, a market maker, or an investor seeking exposure. This is where liquidity becomes critical. Derivatives are easy to define but can be difficult to exit under stress. If there is no willing buyer or seller at the current price, the trade doesn’t happen, or the price must move sharply until balance is restored. This dynamic becomes more important as derivative-like instruments expand into tokenized assets, events, and real-world data. Investors may find positions easy to enter in normal markets but hard to exit when liquidity dries up. The deeper risk is not just adverse price moves in the reference asset. It’s that the market for the exposure itself becomes thin, distorted, or broken. The future may not suffer from a lack of markets. It may suffer from too many markets and not enough real liquidity supply across fragmented markets to support them.

As finance shifts further from ownership to exposure, investors should ask not only “What does this track?” but also “Who is on the other side, and can I get out when it matters?” The growing layers of tokenized products with new leverage, rehypothecation, and interdependencies can create useful flexibility, but they also make it harder to see where real risk sits.

Tokenized finance is not conceptually more complex than traditional finance, which already runs on layers of claims and derivatives. What’s different is the combination of legal, technical, and market-structure complexity wrapped into instruments that often look deceptively simple: a token, a ticker, and a wallet balance. Underneath that simplicity lies a stack of smart contracts, custodians, oracles, and counterparties that may only reveal themselves when something breaks.

Trade & Reference Objects

The same structures used for commodities and interest rates can be applied much more broadly. Once you have a reference object, a payoff rule, a trusted source of settlement, and willing counterparties, almost anything observable can become the basis for a market. That’s a shift. Finance was never limited to direct ownership of assets. It could always create exposure to measurable things. What’s changing now is the ease of doing it through tokens, smart contracts, automated settlement, and 24/7 global markets.

Prediction Markets

Prediction markets are one of the clearest examples of this shift because they make the structure obvious. A prediction market contract is usually not a share of a company, a bond, a commodity, or a currency. It is a claim that pays based on whether some event happens. Will a candidate win? Will inflation fall below a certain level? Will a company file for bankruptcy by a certain date? Will a movie cross a box office threshold?

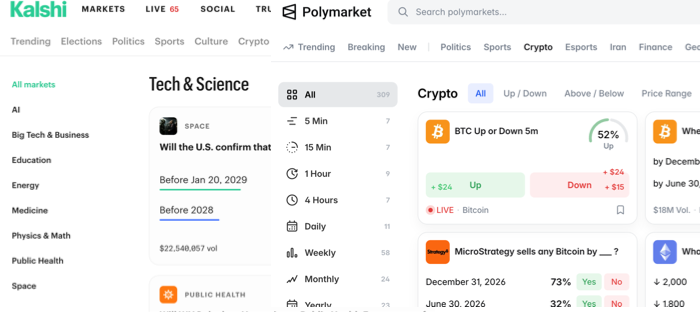

The buyer is purchasing a contract whose payout depends on the event. Mechanically, these markets often use simple binary contracts. A “yes” position may pay $1 if the event happens and $0 if it does not. A “no” position does the opposite. The trading price reflects the market’s current view of the probability, adjusted for liquidity, fees, demand, and participant bias. (See Kalshi and Polymarket.) This is why prediction markets feel like betting, (which – my opinion – is pretty much what they are even if not always legally defined this way), but also resemble derivatives. Prediction markets are economically similar to gambling because users wager on uncertain outcomes. But legally, they may be classified as derivatives, event contracts, swaps, or gambling products depending on the structure, jurisdiction, regulator, and event category. (Legal status is still somewhat in contention in some venues.) In any case, the payoff is derived from an external reference outcome. The key ingredients are not ownership, production, or control. They are event definition, market price, settlement rules, and a trusted resolution source.

Traditional Derivatives

Traditional derivatives are the older and more established version of this same pattern. At a high level, a futures contract, option, swap, or forward agreement gives someone economic exposure to an underlying asset or benchmark. That exposure is often separate from actual ownership. You can trade oil futures without ever wanting physical barrels of oil. You can trade interest-rate swaps without lending money directly. You can buy an option on a stock without owning the stock.

The mechanism is contractual. The parties agree that the contract’s value will change based on the value of something else. Settlement may involve physical delivery in some cases, but it is often simply cash-based, with one party paying the other according to a formula.

This structure creates enormous flexibility. It allows risk to be transferred, hedged, amplified, sliced, bundled, and speculated on. But it also creates abstraction. The further these contracts move from direct ownership, the easier it becomes for people to misunderstand what they actually hold. Many investors today are buying new products without fully knowing what they own or how the underlying information mechanisms work.

Real-World Assets

Real-world assets, or RWAs, are often described as bringing traditional assets on-chain. That can mean tokenized Treasury bills, private credit, real estate interests, invoices, commodities, or other off-chain assets represented through blockchain-based tokens. People are in the process of tokenizing all manner of things from traditional things to your local shopping center to medical data to who knows what comes next. Will there be markets and liquidity for all of these markets? This will be a fascinating question going forward.

In most cases, the token is not the asset. It’s a digital representation of a legal, contractual, or custodial claim connected to an asset. The mechanism usually requires several layers. Someone owns or controls the off-chain asset. A legal structure defines rights to it. A custodian, trustee, issuer, or administrator manages the asset or claim. Tokens are then issued to represent some economic interest in that structure. This can be useful. Tokenization can improve transferability, transparency, settlement speed, and fractional access. But it does not magically eliminate the need for trust. The token holder still depends on legal documents, custody arrangements, redemption rights, regulatory compliance, and the honesty and solvency of intermediaries.

RWAs are not a pure revolution in ownership. They are an extension of representative ownership into programmable rails. Everything still gets back to trust. The important questions are still old-fashioned ones. Who controls the asset, what rights does the token holder have, who enforces those rights, and what happens if the issuer or custodian fails?

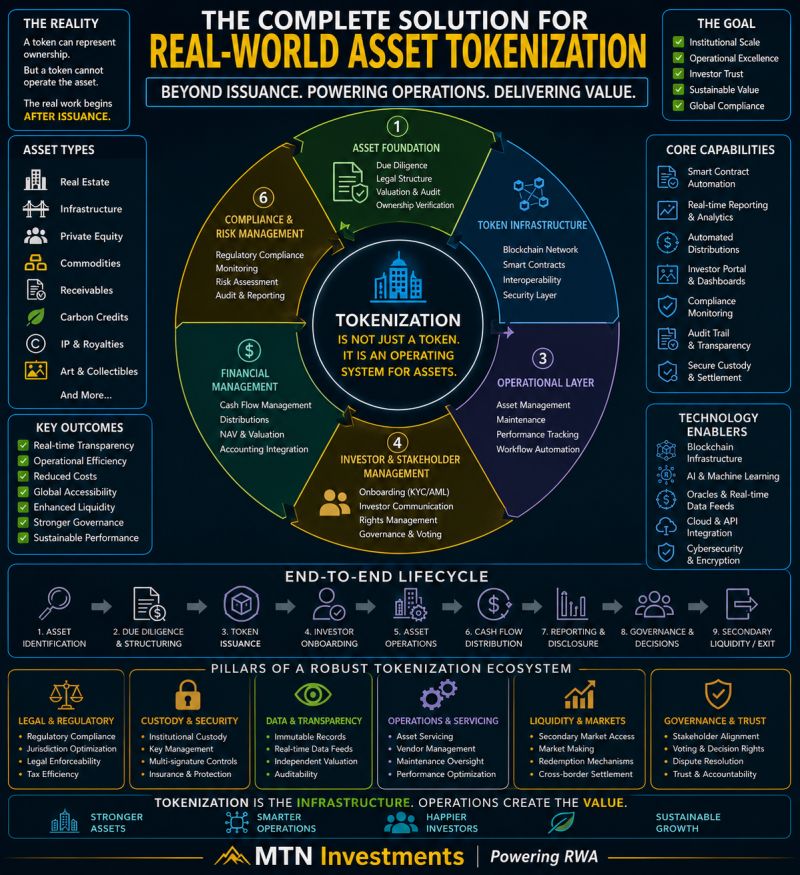

Image from: Tahir Nadeem Chaudhry post on full solution for RWA tokenization.

Stablecoins

Stablecoins are a great example of reference-based finance.

A dollar stablecoin is designed to be pegged to and trade at or near one U.S. dollar. (Or some other reference currency.) The token itself is not a dollar, and it is not the same as a bank deposit. It’s a digital token issued by an entity that promises that the token can maintain dollar value through reserves, redemption, market confidence, and operational controls; for the most part by holding verifiably safe dollar reserves. Though this can be questionable.

As always, the mechanism of such things depends on backing and trust. The issuer may hold cash, Treasury bills, repo agreements, bank deposits, or other reserve assets. Users accept the token because they believe it can be redeemed, traded, or otherwise treated as dollar-equivalent within the relevant ecosystem. This is powerful because stablecoins make dollars programmable and transferable across crypto networks. But it also introduces a layer of representation. The stablecoin is not the reserve asset itself. It is a claim, or at least a market instrument, whose value depends on the quality of the reserves, the issuer’s behavior, the legal environment, and confidence in redemption. This is why stablecoins sit in a middle ground. They can function like money in practice, but structurally they are actually claims on a reference value.

Synthetic Assets

Synthetic assets take the logic even further. A synthetic asset gives exposure to the price of something without necessarily holding the underlying thing at all. A synthetic version of gold, Apple stock, the S&P 500, or Bitcoin can be created through collateral, smart contracts, or agreements that track the reference price.

The mechanism is usually based on collateral and price feeds. A user locks up collateral, the system mints a synthetic asset, and an oracle provides the price needed to determine whether the system remains solvent. If the collateral falls below a required threshold, the position may be liquidated.

This is an elegant but risky structure. It allows markets to create exposure to almost anything with a reliable price feed. But it also means the synthetic asset is only as strong as the collateral system, liquidation mechanism, oracle, market liquidity, and legal framework behind it. Again, the user does not necessarily own the underlying thing at all. They own a constructed financial exposure whose value depends not only on the reference asset or event, but also on whether there is a functioning market, counterparty, or redemption path when they want out.

Tokenized Securities

Tokenized securities are a more regulated version of the same representative logic. A stock, bond, fund interest, or private-market investment can be represented as a digital token. In theory, this can make securities easier to transfer, settle, fractionalize, and integrate with digital systems. But the token does not remove the legal substance of the security. At least, if this is done properly in compliance with real world legal structures, it wraps that legal substance in a new technical form.

The mechanism depends heavily on compliance. Tokenized securities often require identity checks, transfer restrictions, approved wallets, regulated issuers, broker-dealers, transfer agents, custodians, or other intermediaries. Unlike a fully permissionless crypto token, a tokenized security may only be transferable among eligible participants. This is important because it shows the difference between a token and a right. The token may be the technical record of ownership or entitlement, but the actual investor rights still come from securities law, issuer obligations, corporate records, and contractual terms. These are the things that are still being sorted out in legal structures.

Tokenization can improve infrastructure when the token is connected to real legal rights, but it does not magically create those rights. In the best case, it digitizes claims that already exist in law. In the weaker case, it creates a tradable exposure that may depend mostly on smart contracts, collateral, market liquidity, issuer promises, or user confidence. And despite the name, “smart contracts” may have zero basis in law. The code may execute automatically, but that does not mean a court, regulator, issuer, or custodian owes the holder anything. A smart contract can be legally meaningful, legally irrelevant, or legally problematic depending on whether it is tied to an actual legal agreement and whether it satisfies ordinary contract-law requirements. The CFTC’s smart-contract primer makes this exact distinction: a smart contract may not be a legally binding contract, may only be part of a broader contract, and would not be enforceable if it violates the law.

Oracles

Oracles are an underappreciated dependency in many reference-based financial systems, and a potentially risky one. They sound great in theory because they simply deliver information. In practice, they represent a serious point of manipulation. A small change in a measurement can set off large consequences. The traditional stock market has circuit breakers. Worldwide token trading across multiple decentralized exchanges has far less protection.

If a contract pays out based on the price of ETH, the result of an election, the value of a stock, or any real-world event, someone or something must define the official truth. In traditional finance, this role is played by exchanges, index providers, government agencies, courts, or settlement administrators. In crypto, it is often handled by oracle networks or designated data sources. The mechanism is simple in theory. Smart contracts need outside information that blockchains cannot provide on their own, so oracles supply it and contracts execute accordingly. If the oracle is wrong, manipulated, delayed, ambiguous, or disputed, the financial contract may settle incorrectly. Prediction markets highlight this problem especially clearly because event wording is often messy. What exactly counts as “happened”? Which source is official? What if the result is challenged or only partially occurs?

As finance becomes more reference-based, the power to define the reference becomes enormously important. The oracle is not just a technical component. It is the bridge between reality and payout.

The Common Structure

Across all of these examples, the pattern is similar. You don’t always need to own the underlying thing. Actually, mostly you don’t. You need a structure that defines exposure to it. That structure usually has five general parts or some aspects of them: a reference object, a payoff or entitlement rule, a source of truth, an enforcement mechanism, a market or counterparty.

Once those pieces exist, almost anything can be financialized more easily than ever before.

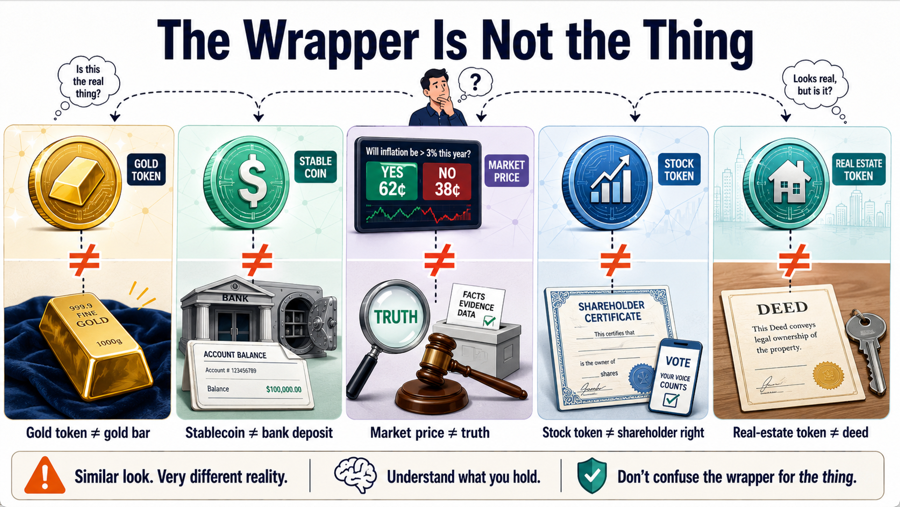

The Wrapper Is Not the Thing

The danger is that people often confuse the wrapper with the underlying thing. A token that tracks gold is not necessarily gold. A stablecoin that trades at one dollar is not necessarily the same as a dollar in a bank account. A prediction market price is not truth. A synthetic stock token is not necessarily a shareholder right. A tokenized real estate interest is not the same as holding the deed to a house. These distinctions may sound obvious once stated plainly, but the evidence from crypto and investor-literacy research suggests many users are not yet crystal clear on the rights, risks, redemption paths, and dependencies behind these instruments. A 2025 Canadian financial-consumer study found that only 21% of respondents could select an accurate definition of stablecoins, and respondents averaged 18% on stablecoin knowledge questions while estimating their own score at 50%. That is pretty direct evidence of overconfidence and misunderstanding.

There is more reason to doubt that investors are fully clear on these distinctions. The International Organization of Securities Commissions (IOSCO) in its 2025 report Tokenization of

Financial Assets has warned that tokenized-asset investors may misperceive what they actually hold. (See Chapter 4, Section B.1: “Representation of Financial Assets in the Form of Tokens.”) The IOSCO report also warns that tokenized-asset structures may not make investor rights to the underlying asset transparent or easily understood. So the question is not merely whether these products can be engineered. It is whether investors understand what the wrapper actually gives them.

These distinctions can sound technical until something goes wrong. The real world still matters. That’s where we still live. When markets are calm, wrappers feel like the thing they represent. When liquidity is deep, the claim feels as good as the asset. When redemption works, the token feels equivalent to cash. When oracles function correctly, the reference price feels objective. When the rising tide lifts all ships, everyone is happy and we all pile in. The fear and greed index pushes to the right.

But stress reveals the difference. My favorite quote about finance and investing is from Warren Buffett. He said something like, “Only when the tide goes out do you discover who’s been swimming naked.” What he meant by that was when conditions are easy, hidden risk can stay hidden; when liquidity dries up or markets turn, you find out who was over-leveraged, exposed, or pretending to be safer than they were.

I think it’s still unclear in some of these newer markets where risk may live; both for individual assets and systemic. Can you redeem? Against whom? Under what law? With what priority? What happens if the issuer fails? What happens if the oracle is wrong? What happens if the market freezes? What happens if the underlying asset exists, but your claim is weaker than you thought?

These are not minor details. They are the substance of the instrument.

Is All of This Good or Bad?

Arguably, potential benefits exist. But there are new risks. Reference-based finance can be useful. It can make markets more efficient, expand access, improve hedging, reduce settlement friction, and allow people to manage risks that were previously hard to trade. Farmers, airlines, banks, insurers, investors, and businesses all benefit from financial instruments that separate exposure from direct ownership. Prediction markets may also produce useful signals. If designed well, they can aggregate information about future events. Stablecoins can move value quickly across digital networks. Tokenized assets can modernize old financial plumbing. Synthetic assets can create access to exposures that might otherwise be difficult to reach.

But abstraction has costs. When one thing represents another, we’re adding flexibility, but also more points of potential failure. There’s more to manipulate. And there’s maybe also more interdependencies we don’t fully see yet. The more layers there are between the user investor and the underlying reality, the more room there is for misunderstanding, leverage, fragility, regulatory confusion, and hidden counterparty risk. A simple asset can become a complex chain of promises.

The question is whether investors can still understand what they actually own and evaluate accordingly.

The Regulatory Problem

Regulators struggle with these products because the same economic structure can resemble different legal categories depending on design. A prediction market may look like a derivative, a gambling product, an information market, or a public-interest forecasting tool. A token may look like a commodity, security, payment instrument, fund interest, deposit substitute, or contractual claim. A stablecoin may look like money to users, but like an issuer liability to regulators. A synthetic asset may look like a derivative even if it is implemented through decentralized smart contracts.

The law is trying to define things by their structure, rights, marketing, control, jurisdiction, settlement, issuer promises, and user expectations. It’s not enough to say something is “just a token”. Neither is “it’s just a bet.” The question is: what rights does the holder have, what determines the payout, who is obligated, who controls settlement, and what happens if the system breaks?

The Financialization of Reality

The deeper trend is that finance is moving from what was mostly simpler assets to references. If something can be measured, verified, priced, and settled, it can potentially become a market. Not because the market owns the thing, but because the market can create exposure to the thing. And there’s plenty of folks who want to package these things up and sell them.

This is among the reasons prediction markets are more than a niche curiosity. They’re a visible example of a much broader movement. They show how facts, events, expectations, and outcomes can be turned into tradable contracts. Crypto accelerates this because blockchains make it easier to issue tokens, automate settlement, compose financial instruments, and move value globally. But crypto did not invent the underlying idea. It inherited and expanded a long tradition of representative ownership and derivative exposure.

The old world gave us deeds, receipts, bank balances, stock certificates, futures contracts, and swaps. The new world is giving us stablecoins, RWAs, synthetic assets, tokenized securities, oracle-driven contracts, and prediction markets. The pattern is essentially similar. It’s just the ease of the mechanisms can make the scope much wider.

Bottom Line

So, is everything going to be a derivative?

Not literally. At least probably not. Some things will still be owned directly. (Probably. I say this now, and then two years from now somehow someone will prove me wrong.) Companies will still issue equity. Goods will still be bought and sold. Cash, commodities, and property will still matter. My assertion is we still live in the real world. Eventually, things have impact here. Some new trading mechanisms and payment rails will live in agentic workflows or other structures. But for us? Can I afford to live in my home? How much are groceries? I don’t think it’s going out on a limb to suggest these will remain the top concerns as they always have. Still, it’s seeming like more of the economy will be mediated through instruments that provide exposure rather than direct ownership. More assets will be wrapped. More claims will be tokenized. More events will become tradable. More prices will be referenced. More real-world facts will be pulled into financial contracts.

The future may not be that everything becomes a derivative. The future may be that everything becomes capable of having a derivative built on top of it. And once that happens, the most important question for users, investors, regulators, and builders will not be simply, “What does this track?”

It will be What do I actually own?

Some Questions for a Checklist

- What does this instrument actually give me?

- Is it ownership, a legal claim, a redemption right, or just price exposure?

- Who is the issuer or counterparty?

- What source determines the reference value?

- What happens if liquidity disappears?

- What happens if the issuer, custodian, oracle, or market fails?

- Will I be able to redeem, sell, or settle under stress?