Consumer protection in Web3 has come a long way, but it’s still nowhere near what you’d get from a traditional bank or broker. Billions in losses from hacks, rug pulls, and failed platforms tell a story that headlines alone can’t fully capture.

Some frameworks are in place now, and more are taking shape. But the gaps are significant, and they affect you directly.

This post breaks down what protections actually exist in Web3 today, where they fall short, and what you can do to protect yourself while the rules keep catching up.

This article is mostly for ordinary users and investors trying to understand what protections they actually have before using exchanges, wallets, tokens, or DeFi protocols. However, it’s also useful for those building in Web3, because these unresolved protection gaps are the kinds of issues that shape user trust, investor confidence, and adoption decisions.

The State of Consumer Protection in Web3 Right Now

The biggest regulatory move in recent years came from the EU, though in mid-2026 the U.S. is catching up fast. Europe’s MiCA, the Markets in Crypto-Assets Regulation, reached fuller implementation in 2025 as enforcement and transitions phased in. Under MiCA, Crypto-Asset Service Providers (CASPs) like licensed exchanges, custodians, trading platforms, and other crypto-asset service provider platforms must meet certain capital requirements. They must also follow governance rules and give users clear disclosures on fees, risks, and redemption terms.

Now the US has also made significant progress. The GENIUS Act became law in July 2025, putting a federal framework in place for stablecoin issuers. The CLARITY Act has moved forward in Congress too. A full market structure law covering the broader crypto market hasn’t fully passed as of May 2026 as it winds through Congress, so there are still gaps, but this seems to have bipartisan support and getting it the rest of the way done is mostly about details. (See more at Crypto Legislation 2026: Key Laws Reshaping Digital Assets.)

Globally, more jurisdictions are moving toward shared standards on consumer disclosure, anti-money laundering (AML) controls, and market integrity. Crypto is increasingly being treated as a mainstream financial product rather than a legal grey area. This stands to reason as things like real world asset tokenization become more common. No one’s going to be able to sell it if mass market consumers don’t sense they have reasonable protections. Still, more purist Decentralized Finance (DeFi) is the big exception. Most decentralized finance protocols sit outside these frameworks entirely, and no reliable enforceable global standard exists for them yet. (Some might fairly argue this last point, but there’s a difference between just having laws and the actual ability to reliably enforce them.)

Where Web3 Consumer Protection Still Falls Short

MiCA and the GENIUS Act are steps in the right direction, but losses in Web3 haven’t slowed down.

According to Beosin’s Global Web Security Report, Web3 users lost $2.51 billion to hacks, phishing scams, and rug pulls in 2024 alone.

Image via Beosin

In 2025, the numbers got worse. The collapse of the Mantra (OM) token wiped out an estimated $5.5 billion, accounting for roughly 92% of all rug pull losses that year, according to DappRadar. Though this might have been more of a dramatic price crash from liquidation issues vs. a classic developer draining “rug pull.” The team pushes back on the idea of malfeasance on their part, but regardless, a billion here or there adding up to over $5 billion seems like more than just pocket change. A Mantra Co-founder posted multiple times on X explaining that the crash resulted from “reckless forced liquidations” by centralized exchanges (especially during low-liquidity weekend hours). He explicitly denied team involvement, insider selling, or a rug pull. This pushback framed the event as a liquidity cascade/market mechanics failure rather than malice or exit scam. Skeptics still call it suspicious (given supply concentration and timing), but on-chain data largely supported the idea that there were no major team dumps during the initial crash. I’m not sure if that’s all that satisfying though, is it? If it was malfeasance, then we could say, “ok, this was just some more bad guys doing bad things.” But if the defense is that, “Hey, you know what? These structures are either brittle or dependent enough that this just happens sometimes,” is this actually better? (Spoiler alert: No. Probably not.)

Let’s say as a general investor you don’t really care if this was outright malfeasance or a structural design failure. While the team strongly denied any wrongdoing and pointed to reckless liquidations on centralized exchanges as the trigger, the episode still delivered a painful reminder: in Web3, even projects that play by the rules can experience catastrophic drawdowns. Thin liquidity, leveraged positions, and – usually – irreversible on-chain mechanics mean losses can happen faster and with less recourse than in traditional markets.

The Mantra case shows why checking team transparency isn’t enough. Smart buyers also look at tokenomics: vesting schedules, circulating supply, liquidity depth, and how much of the token is actually tradable without triggering a cascade. If the economics look fragile, even a great idea can turn into an expensive lesson. By the way, among those items, liquidity depth might start being increasingly important. It might be common to say things are only really worth what people are willing to pay for them. However, we really have to add “willing to pay for them at a particular time.” For example, if you tokenize some asset and make it available 24/7, that seems to have value. Or at least some claim so. However, even worldwide are there a lot of traders exchanging on Sunday overnights? Maybe. Maybe some agents / bots.

Now… in fairness, it’s not like TradFi (Traditional Finance) hasn’t had its blowups. Archegos Capital in 2021 with one single family office’s leveraged bets triggering $10B in bank losses, LTCM in 1998 trashing a global system with bad levered bets, SVB in 2023 wiped out from a bank run; though in this case FDIC stepped in. Still, Crypto – for now – is arguably worse in both speed and severity. There’s also generally more permanence. On the positive side, Crypto events don’t yet trigger global meltdowns. And Crypto is getting better fast now that more regulations and guidelines are coming along with at least a little bit of market maturity.

The lesson from both worlds is the same: excessive leverage + thin liquidity = trouble. Or at least potential trouble. Crypto just serves it up faster and with fewer seatbelts.

Image via DappRadar

Part of what makes this so difficult is that crypto transactions are generally final once confirmed, which for some users is actually part of the selling point. From another perspective, though, there is usually no dispute process, no chargeback, and no guarantee of recovery if something goes wrong. If funds reach a fraudulent address, getting them back is rarely possible unless the recipient or an intermediary can return them. You may have heard of rare cases where a blockchain community came together and forked a chain after a major exploit, such as Ethereum after the 2016 DAO hack. But that is an extraordinary network-level event, not something likely to happen for an individual mistaken or fraudulent transaction.

DeFi adds another layer to this. Most decentralized protocols have no central authority, which means there’s no regulator to file a complaint with and no equivalent of a financial ombudsman. If a protocol gets exploited, users are largely on their own.

Then there’s the jurisdiction problem. Crypto operates across borders, but regulations are still national. That fragmentation creates gaps that bad actors know how to use, and it makes cross-border enforcement genuinely difficult.

How to Protect Yourself as a Web3 Consumer

Regulation is catching up, but it’s not there yet. Your own due diligence is still your strongest line of defense. Here’s what that looks like in practice when looking at projects, coins, investments, etc.:

Check if a platform is licensed: If you’re using a centralized exchange in the EU, verify it holds a MiCA license. In the US, check for registration with the SEC or CFTC. Though some, such as spot crypto exchanges, might be under state money-transmitter licenses. Licensed platforms are subject to consumer disclosure rules and regulatory oversight. (ESMA Databases and Registers, MiCA section. In the U.S. you may have to try searching a few different places. There’s still not a clear single database as yet. Licensed platforms still aren’t risk-free of course (hacks can happen), but they must follow capital rules, disclosure requirements, and face real oversight which should dramatically improve your odds compared to unlicensed operators.

Example: Your brother’s third cousin’s friend just got out of college and is visiting before they all start their first career jobs. They are, of course, long time crypto traders. Over three years now in fact. Experts if ever there were. And they swear by the Bitstamp exchange. But you want to check.

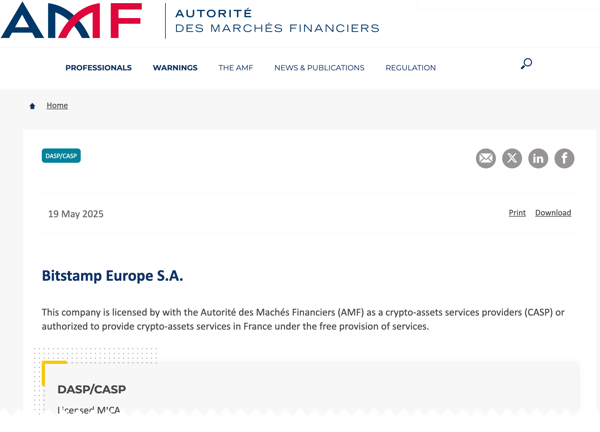

In Europe, use the official ESMA MiCA register or the relevant national regulator’s whitelist. For example, to check a less mainstream exchange like Bitstamp Europe S.A., you can look it up on France’s AMF whitelist, which shows that it has a MiCA license from Luxembourg’s CSSF and is authorized to provide crypto-asset services in France.

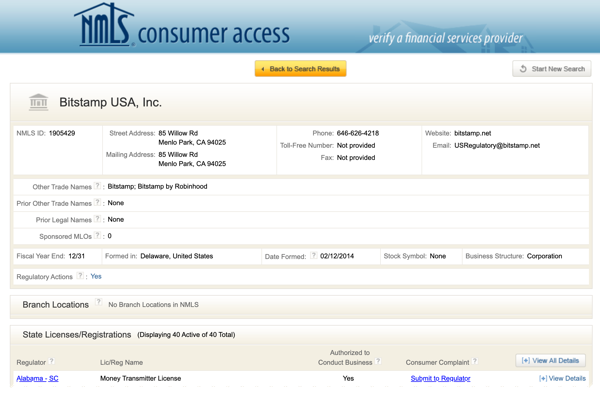

In the U.S., there is no single clean crypto-license database, so start with the company’s legal entity and check NMLS Consumer Access for state money-transmitter licenses; for example, Bitstamp USA Inc. lists NMLS #1905429, which users can cross-check through NMLS. For futures, swaps, or derivatives-related crypto products, use the CFTC’s “Check Registration” page, which points users to NFA BASIC. And again, some organizations may be regulated at a state level. Ideally this will become clearer.

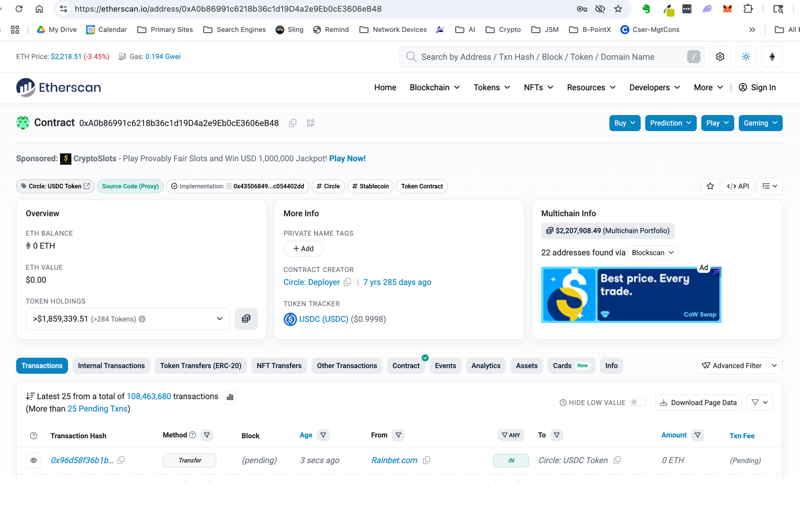

Verify smart contracts before you interact: You don’t have to be an expert Web3 programmer. You can still check some basics. Look for audit reports from firms like Hacken’s audit reports or check a project’s security score on CertiK’s Skynet. Unaudited smart contracts are one of the most common entry points for exploits. On the project’s official website, docs, or dApp, locate the contract address (it looks like a long string of 0x… characters). (Always double-check it against official sources (Twitter/X, Discord, or verified docs) to avoid phishing fakes.) Go to the relevant explorer for the chain you’re using: Ethereum / Layer 2s → Etherscan.io, BNB Chain → BscScan.com, Solana → Solscan.io or others. Paste the address in and look for things like “Contract Source Code Verified” See if there’s audit reports via Google. Even all this doesn’t necessarily mean everything is fine, but it’s a good base level of due diligence.

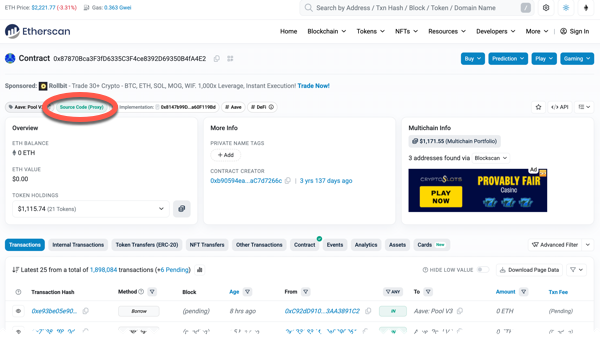

Example: You want to use Aave V3 on Ethereum. Aave’s own docs say the Pool contract is the main user-facing contract for actions like supply, withdraw, borrow, and repay. From Aave’s official address resources, you would confirm the correct Ethereum contract address, then paste that address into Etherscan. On the Etherscan page for Aave’s V3 Pool contract, you can see that the source code is verified, that it is a proxy contract, and that there is a linked implementation contract.

Now, for those playing at home, if you actually went to Aave’s official addresses, and then to the Pool address on Etherscan, you might be confused. Because it’s not there. Or rather, it may not be obvious on the default visible addresses page. At least as of this writing. I was just trying to make a quick example and got stumped myself. (Which is in some ways kind of good. We learn more sometimes when things go a bit wrong. And this helps me give better advice.) In this case, Aave’s Pool docs also explain that the Pool is the main user-facing contract and that it is a proxy owned by the market’s Pool Addresses Provider, which is why there is some indirection. The actual address then, is buried in a GitHub link here.

Most normal people will not go this deep. And no, it shouldn’t be this challenging. But this is how this world works sometimes. Let’s cut to something more realistic for most people. If you are checking a protocol like Aave, you may find that the address is not listed in one obvious place because larger protocols often use complicated structures like proxy contracts, registries, and address-book packages. In that case, do not rely only on Etherscan labels. Cross-check the address against the project’s official docs, GitHub address book, or app-linked documentation. If you cannot confidently match the contract address back to an official project source, pause before connecting your wallet or approving token permissions. Or, (which is what most will likely do), just make sure you’re at the correct URLs for when you’re doing things. But if you’re interacting with contracts for whatever reason? You probably should go to the effort to check at least the first time. Just once. Think of it like when you get spam email with links to a website where you maybe have an account. At this point, sadly most people know these should not be trusted. You look very carefully at the URL that’s getting linked. You’ll ideally see when there’s a clever misspelling or something. This is really just the crypto / decentralized finance version of this. Check the address. Then make sure anything else you do is only with that address. Also, be careful copying addresses from your transaction history. These addresses are long and cut / paste is an obvious and sensible shortcut to not mess up the address. However, scammers sometimes use address-poisoning attacks, sending tiny-value or zero-value token transactions from lookalike addresses so the fake address appears in your wallet activity. Because wallet addresses are long and awkward to verify, they hope you later just casually go into your wallet history and copy the wrong one by mistake and use it to send funds.

After all this, none of it proves the contract is safe, but it is a useful sanity check that it’s from a legitimate source; or at least the source you intend to use. You can then look for audit information from the project itself. In this case, Aave has a public security page with official audit reports and independent security reviews. If you cannot find a verified contract, cannot match the address to the project’s official docs, or cannot find any credible audit history, treat that as a serious warning sign before connecting your wallet or approving token permissions.

Check wallet and token addresses: Use block explorers like Etherscan, Polygonscan, BscScan, or Solscan to verify addresses before any transaction. Phishing sites often use near-identical interfaces to trick you into sending funds to a fraudulent address. Are block explorers totally unfamiliar to you? Here’s some beginner friendly videos: Block Explorer Tutorial – Walkthrough Etherscan, Polygonscan, Solscan, and How to Use Etherscan and Solscan: Blockchain Explorer Tutorial 2026.

Example: This one should be relatively easy. Suppose you want to receive or send USDC on Ethereum. Do not just trust the ticker symbol “USDC,” because fake tokens can use the same name and logo. Circle’s official USDC contract-address page lists the Ethereum USDC token contract as 0xA0b86991c6218b36c1d19D4a2e9Eb0cE3606eB48, and the matching Etherscan page labels it as Circle: USDC Token with verified contract code.

Revoke permissions you no longer need: Revoke.cash shows which dApps have access to your wallet. Review these regularly and remove access for platforms you no longer use. (Note that for some transactions or even to look at things, you sometimes give permissions to sites to work with your wallet. This can just linger on unnecessarily. If there’s no need for that, get rid of such things. You can always re-connect later if wanted.)

Consider self-custody where possible: Keeping assets in a non-custodial wallet means no exchange failure can freeze your funds. The FTX collapse in 2022 is still the clearest example of why this matters. There are other risks to self-custody though. (See Solving Physical Risks of Holding Crypto, Web3 / DeFi Trust Deep Dive, Hidden Stablecoin Trade-Offs) Some argue you’re safer with custodial custody. Purists say the whole point is so you’re in full control of your assets. You make the call one way or the other or some balance of both.

Research the team: For crypto projects, look for doxxed founders, published audits, and a clear roadmap before committing any funds. Anonymous teams with no track record are a higher risk. (So in this case, “doxxed founders” is meant as a positive due-diligence signal as the team info is known and published. Of course, it also makes them targets, but at least you know with whom you’re doing business.)

What Regulators Still Need to Figure Out

DAOs, or Decentralized Autonomous Organizations are one of the clearest unresolved governance gaps. Courts and regulators have started applying older legal categories, such as partnerships, unincorporated associations, securities law, and commodities law, but there is still no settled framework for who is accountable when DAO governance leads to losses, exploits, or unlawful activity. When a DAO makes a bad call or a protocol gets exploited, there’s still no clear legal answer on who’s accountable. And even if there were, it might be challenging or practically impossible to enforce an action.

Regulators are increasingly asking these questions, but no jurisdiction has a satisfying answer yet.

On the more promising side, on-chain analytics is becoming a serious compliance tool. Authorities and firms are using blockchain data, including AI-assisted monitoring, to detect fraud and flag suspicious activity before it escalates.

Consumer disclosure requirements are also improving. MiCA already mandates clear disclosures on fees, risks, and redemption terms, and more jurisdictions are moving in that direction.

Wrapping Up

Web3 consumer protection is no longer an empty promise. MiCA, stablecoin legislation, licensing regimes, disclosure rules, audits, analytics tools, and better compliance practices all point in the right direction. The industry is maturing, and regulators are no longer treating crypto as some fringe experiment outside the financial system.

But that does not mean Web3 users are protected in the way bank customers or brokerage clients are protected. Not yet.

The biggest risks remain structural. Irreversible transactions, thin liquidity, opaque tokenomics, cross-border enforcement gaps, smart contract exploits, phishing, wallet-draining permissions, and DeFi protocols with no obvious party to hold accountable. Even when there is no fraud, users can still suffer massive losses from brittle market mechanics or poorly designed incentives.

This is the uncomfortable middle ground Web3 occupies today. It is safer than it used to be, but not safe enough to treat as casually as one might more traditional financial instruemnts.

For ordinary users and investors, the takeaway is simple. Assume that upfront responsibility is more important than recourse, because oftentimes, there’s still no practical recourse for some problems. Check licenses. Verify contracts. Understand custody. Review permissions. Look at liquidity, token supply, audits, and team transparency before committing funds.

For builders, the lesson is just as important. Consumer protection is not only a regulatory burden. It is becoming a product requirement. The projects that earn trust will not be the ones that merely say “decentralized” or “transparent.” They will be the ones that make risks understandable, controls usable, and accountability credible. How many people do you think are really going to go through the Aave verification steps above? It’s all still a bit much effort for many to easily and safely participate.

Web3 may eventually offer stronger, faster, and more open financial systems. But until its protections catch up to its promises, the first line of defense is still an informed user.