Crypto legislation in 2026 is finally catching up with the market.

The US now has its first federal stablecoin law on the books. Europe’s MiCA framework hits its final enforcement deadline in July. And crypto tax rules in the US are being rewritten.

These are active regulations that affect the tokens you hold, the platforms you use, and how you report your trades. There are some that are not wholly operational as yet in terms of operational deadlines, so we’re still seeing these roll out; sometimes with comment periods extended. Still, a great deal of regulatory ambiguity is getting cleared up.

This post breaks down the biggest developments, where each one stands right now, and what you should consider doing with the information.

The U.S. Moves Toward a Clearer Crypto Rulebook in 2026

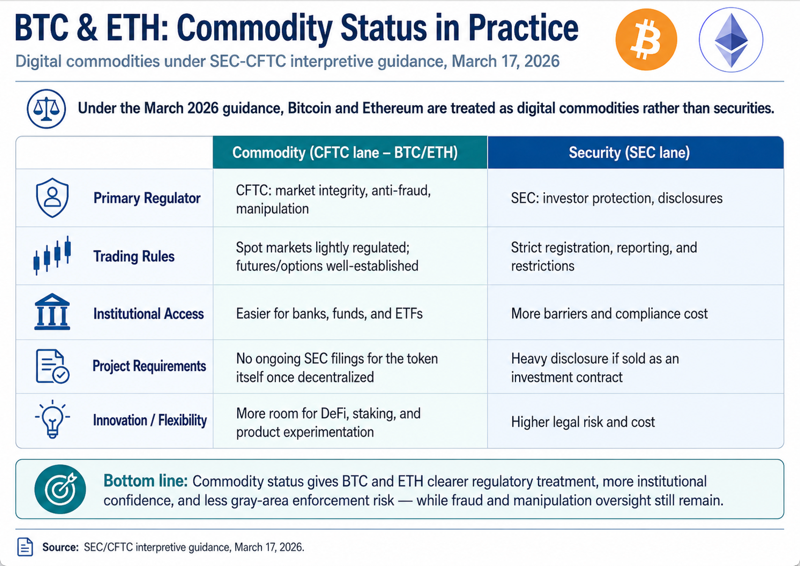

For years, the SEC and CFTC both claimed jurisdiction over crypto assets. That overlap created real problems for the industry. Exchanges, projects, and investors had no clear rulebook to follow. Most have likely heard of the SEC. (The Securities and Exchange Commission). This is the primary federal agency that regulates securities markets, protecting investors and maintaining fair, orderly, and efficient markets. Just in case you’re not as familiar with the CFTC, it’s the U.S. Commodity Futures Trading Commission, an independent federal agency that oversees the country’s derivatives markets. Think futures contracts, options, swaps, and anything tied to commodities (from traditional ones like oil, gold, and agricultural products to newer digital assets).

In the context of the legislation we’re talking about here, the CFTC is one of the two key U.S. regulators for digital assets (alongside the SEC). Here’s the practical split that’s becoming clearer this year:

- CFTC jurisdiction → Digital commodities like Bitcoin and (in most cases) Ethereum. This covers spot markets, futures, and anti-manipulation rules.

- SEC jurisdiction → Tokens that look more like securities (investment contracts under the Howey test).

Regarding CFTC vs. SEC, this jurisdictional confusion began changing in 2025 when the US Congress passed the GENIUS Act, the first major US law built specifically for crypto. But passing a law and enforcing it are two different things.

In January 2026, the SEC and CFTC launched Project Crypto, a joint initiative to coordinate oversight and build a unified approach to digital asset regulation. Project Crypto started as an internal SEC effort in 2025 but was officially relaunched on January 29, 2026 as a joint SEC-CFTC initiative. The event at CFTC headquarters marked the shift from separate agency work to coordinated oversight

Then in March, both agencies signed a Memorandum of Understanding, committing to “clarify, coordinate, and harmonize” their policies on crypto assets.

By April, the SEC had formally ended its enforcement-first approach, withdrawing several prior actions against crypto firms.

The message was that the previously adopted “regulation by punishment” stance was giving way to a more functional “regulation by rules.”

Howey Do You Do

I’m sure this obvious pun has been used. But there you go. The Howey Test might be somewhat known at this point, (certainly by those working in finance), but it bears mentioning here for general completeness. Why are Bitcoin and Ethereum classified as “digital commodities?”

The key test comes down to the Howey Test (the Supreme Court standard for what counts as a security/investment contract). It goes back to a 1946 Supreme Court case and may be worth checking out the Wikipedia link just for some historical context. The effect now, decades later, is this: A token is a security if buyers expect profits primarily from the “essential managerial efforts of others” (like a centralized team promising to build something valuable). The March 2026 SEC/CFTC interpretation provides the clearest federal guidance yet that major crypto assets such as Bitcoin and Ethereum can be treated as non-security crypto assets, or digital commodities. But that does not mean every transaction involving BTC, ETH, or similar assets is automatically outside securities law. The asset itself may be treated as a digital commodity, while a specific sale, staking program, wrapped product, yield arrangement, or packaged investment deal could still create securities-law issues depending on how it is marketed, managed, or structured.

- Bitcoin: It’s the purest example. No issuer, no pre-mine, no company behind it. Its value comes purely from the decentralized network running via proof-of-work, global supply/demand, and its role as digital money. The CFTC has called it a commodity since 2015, and the 2026 guidance reaffirms this.

- Ethereum: It launched with a pre-sale (which could have looked securities-like early on), but the network is now fully functional and sufficiently decentralized. Therefore, value derives from the programmatic operation of the blockchain (smart contracts, staking, gas fees, etc.) plus market dynamics, not from any single team’s ongoing efforts. The joint guidance explicitly lists ETH alongside BTC as a digital commodity.

Just as a comparison: These assets behave like digital gold or oil. Their worth is driven by the network’s utility, scarcity, and what people are willing to pay, not promises from a CEO or dev team.

Note that some aspects of Ethereum may not always fit cleanly as a commodity though. Yes, the ETH token itself is a non-security digital commodity because its value comes from the decentralized, programmatic operation of the Ethereum network. However, here are the practical situations where ETH (or related activities) can still bump into securities rules. There could be specific sales or offerings that create an investment contract, which would be a security. The token would stay a commodity, but the transaction could then fall under SEC rules. Then there’s the idea of “wrapped” or “derivatives” of ETH which could cross a line if they introduce new promises of profits from some team. It can still be problematic in terms of staking rewards or airdrops, because they might not be a security under the new rules if they’re fully decentralized in terms of participation, but if there’s something like staking pools with manager promises, that could cross a line.

So… there’s more clarity. However, you do have to watch for how something is marketed or packaged in a deal that could turn it into a potential security.

What the GENIUS Act Means for Stablecoin Users

Earlier I’d said the US now has its first federal stablecoin law on the books. It may be that it’s “on the books” in that the GENIUS Act is now law, but many operating requirements are still being implemented through agency rulemaking. So the framework is on the books, but not every obligation is fully effective yet.

The Guiding and Establishing National Innovation for US Stablecoins Act, better known as the GENIUS Act, passed with strong bipartisan support. This law is almost entirely about stablecoins. Recall that a stablecoin is a type of cryptocurrency engineered to hold a steady value, most commonly pegged 1:1 to a traditional fiat currency like the US dollar, so it can be used for everyday payments, trading, and value transfer without the wild price swings typical of Bitcoin or Ethereum. Basically, stablecoins are the practical “digital dollars” of the web3 world. They’ve become the bridge that lets businesses and users move money on-chain with confidence and minimal volatility.

Anyway, the legislation cleared the Senate 68–30 and the House 308–122. That kind of margin signals durable policy, not a narrow political win.

Still, not everyone was on board. While the GENIUS Act passed with strong bipartisan support, it still faced notable opposition. Critics argued the bill didn’t go far enough on consumer protections, anti-money laundering safeguards, and measures to protect financial stability. Some warned that the framework around foreign stablecoin issuers could reopen risks seen in earlier collapses. Others raised concerns about potential conflicts of interest involving politically connected crypto projects. A separate group of lawmakers worried the rules gave too much leeway to large tech platforms that might issue their own stablecoins and collect extensive user financial data. These debates didn’t stop the bill from becoming law, but they help explain why regulators are still finalizing detailed implementation rules, and why businesses should stay alert as those guardrails take shape.

The law sets three core requirements for any stablecoin issuer operating in the US:

- Issuers must hold 100% reserves in high-quality liquid assets at all times.

- They must obtain a federal license before issuing any payment stablecoin. There’s both federal and state qualifying pathways, plus different categories of permitted payment stablecoin issuers.

- They must submit to regular independent audits to verify their reserves. (likely monthly public disclosures.)

For anyone holding USDT, USDC, or similar dollar-pegged assets, this delivers real legal clarity. The risk of an issuer quietly mismanaging reserves, the kind of failure that contributed to past collapses, becomes much harder to hide under this framework.

One area to watch is stablecoin yield. In February 2026, the Office of the Comptroller of the Currency proposed rules that could restrict platforms from offering rewards on stablecoin holdings.

If those rules are finalized as proposed, earning yield on stablecoin balances at exchanges like Coinbase could become significantly limited.

The CLARITY Act and the SEC vs. CFTC Question

The Digital Asset Market Clarity Act, or CLARITY Act, passed the House in July 2025 with bipartisan support. As of May 2026, it is still working its way through the Senate.

The core problem it aims to solve is one that has frustrated the industry for years. That problem is two regulators claiming authority over the same assets, with no clear boundary between them.

The CLARITY Act would sort digital assets into three categories:

- Digital commodities like Bitcoin and Ethereum would fall under the CFTC.

- Securities-like tokens would stay with the SEC.

- Permitted payment stablecoins already covered by the GENIUS Act would sit in their own category.

That structure gives investors a much clearer map of which assets carry regulatory risk and which do not.

The bill also proposes a joint SEC-CFTC innovation sandbox, giving blockchain projects a space to test new products under regulatory supervision.

If it passes, it could open the door to significantly more institutional participation in crypto markets.

Hold On… Where Did Stablecoins Go?

Ah, you’re wondering, “OK, so who regulates Stablecoins?”

That would be existing banking regulators.

Under the GENIUS Act, payment stablecoins operate in their own dedicated category, regulated primarily by federal banking agencies such as the OCC, FDIC, and Federal Reserve, not the SEC or CFTC. The CLARITY Act recognizes and reinforces the GENIUS framework. So the FDIC (Federal Deposit Insurance Corporation) helps supervise certain permitted payment stablecoin issuers. And the OCC (Office of the Comptroller of the Currency) which is the primary regulator for national banks and federal savings associations, issues federal licenses to stablecoin issuers, sets the detailed rules for 100% reserves, audits, redemption rights, capital requirements, and risk management. It’s sensible to think of the OCC as the main “banking rule writer” for the new GENIUS Act framework, though this is shared across federal banking, credit union, Treasury, and state regulators. Together, these two agencies (along with the Federal Reserve) give stablecoins a dedicated banking-style regulatory home separate from the SEC and CFTC. This is what makes the GENIUS Act feel like real progress: stablecoins can now treated more like trusted financial instruments than wild speculative tokens.

Summary:

- OCC = issues the license and writes the operating rules.

- FDIC = supervises FDIC-regulated stablecoin issuers and custodians, helps set prudential rules, and clarifies how deposit insurance applies to reserve deposits. Stablecoin holders should not assume their tokens are FDIC-insured.

- Others: There are additional regulatory agencies: NCUA (National Credit Union Administration), and state regulators where applicable.

MiCA Takes Full Effect in Europe

The Markets in Crypto-Assets Regulation, or MiCA, is the EU’s comprehensive crypto framework covering all 27 member states. And July 1, 2026, is its hard deadline.

From that date, any crypto service provider operating in the EU without a MiCA license must cease EU operations entirely.

For crypto service providers, MiCA sets three baseline requirements:

- Full authorization from a national regulator before offering any crypto services in the EU

- Governance structures and operational risk management meeting EU standards

- Full anti-money laundering (AML) compliance, including transaction monitoring and customer due diligence

Providers operating without authorization after July 1 may face forced wind-down, client offboarding, supervisory action, and significant penalties depending on the violation and member state.

On the stablecoin side, USDT has already been delisted from several major EU platforms, including Coinbase EU and Binance EEA, as Tether has not yet met MiCA’s reserve and disclosure requirements.

USDC and euro-backed stablecoins are currently better positioned for EU compliance. Why? Circle (the company behind USDC and EURC) actively pursued and obtained MiCA authorization through a French Electronic Money Institution (EMI) license. This allows them to legally issue and distribute both USDC and their euro-pegged token (EURC) across the entire EU under the “passporting” system. Tether (issuer of USDT) has publicly chosen not to apply for MiCA licensing. Their CEO cited concerns over requirements like holding a large portion of reserves in European banks, which they viewed as risky or incompatible with their global model. Because of the above, major EU platforms (Coinbase EU, Binance EEA, Kraken, etc.) have delisted or heavily restricted USDT for European users to avoid regulatory risk after the July 1, 2026 deadline. Meanwhile, USDC and compliant euro stablecoins (EURC, EURI, etc.) remain fully available and are seeing increased adoption.

Crypto Tax Rules Are Changing Too

The IRS has been applying its 2014 guidance on digital assets, which treats every crypto disposal as a taxable event. That includes swaps, staking rewards, and even spending stablecoins on everyday purchases.

In December 2025, Representative Max Miller released the bipartisan discussion draft Digital Asset PARITY Act to address some of the biggest friction points for retail users. Supporters are aiming to move some version of the proposal in 2026, but it remains pending and may change. Here’s a summary from one of the bill sponsors, Congressman Max Miller.

The bill proposes three changes worth knowing about:

- A de minimis exemption for stablecoin transactions under $200, meaning small purchases would not trigger a taxable event

- A five-year deferral on taxes owed from staking and mining rewards

- The application of wash sale rules to crypto, which would prevent selling a token at a loss and immediately buying it back to claim the deduction

One thing that is not waiting for reform is broker reporting. New requirements for crypto brokers came into effect in 2026, adding more complexity to tax filing.

The Bottom Line

The regulatory picture is getting clearer, but there are still moving parts. With the GENIUS Act, MiCA, and the CLARITY Act still working through the Senate, 2026 is the year crypto regulation moves from discussion to enforcement.

Here is what you can act on right now.

- Check which stablecoins you hold and where you hold them. GENIUS Act implementation rules are due July 2026, and the yield program debate could affect what your exchange is allowed to offer.

- If you use a platform that operates in the EU, verify it holds a MiCA license before July 1. Unlicensed providers have no legal right to serve EU users after that date.

- Keep an eye on the CLARITY Act as it moves through the Senate. If it passes, it will directly affect the regulatory classification of tokens in your portfolio.

- Record every trade, including swaps and staking rewards. Broker reporting rules are also changing, adding more complexity to digital-asset tax filing as implementation phases in, and tax reform is not finalized yet. If you’re not already using one, consider finding a tax reporting tracking service. They’ll certainly be keeping up on the regulations. They can help you track and fill out some of the right forms at tax time, either for yourself or to provide to your accountant.

See Also:

- GENIUS Act: Full Law

- GENIUS Act: Congress.gov bill summary & status page

- GENIUS Act: White House Fact Sheet

- H.R.3633 – Digital Asset Market Clarity Act of 2025 (Full Text)

- H.R.3633 – Digital Asset Market Clarity Act of 2025 (Summary & Status)

- CRS Insight: An Overview of H.R. 3633, the CLARITY Act – Excellent explainer

- MiCA – Regulation (EU) 2023/1114 – Official Text (EUR-Lex) (full)

- ESMA – Markets in Crypto-Assets Regulation (MiCA)

- MiCA Summary of All Texts & Delegated Acts