Note: the primary discussion here is about basic, issued fiat reserve backed stablecoins, not algorithmic or any other types of stablecoins.

Stablecoins may be the first truly mainstream useful thing to come out of crypto. Here’s a deep dive into some things to be aware of though…

First, why should you care about anything written here? Stablecoins matter because they may be crypto’s first broadly useful product at scale. But they are often misunderstood. Many people think they are simply “digital cash on-chain.” In practice, they are usually privately issued, reserve-backed, compliance-constrained financial instruments with token interfaces. That makes them powerful and also means they inherit legal, banking, liquidity, and control-point realities that many users and even some builders don’t fully account for.

Many consumers, and even some crypto product builders, understand stablecoins at the price peg layer, but not at the control points, redemption mechanics, and compliance constraints layer.

We should always know what we’re buying and what assets we’re holding. Stablecoins are useful and increasingly foundational to crypto payments and settlement. Crypto traders may hold a fair amount of stablecoins as they use them as a basis currency for trading. They’re a way to park value without going back to fiat, and manage collateral / margin.

Stablecoin. The name itself inspires confidence. Something to be aware of, though, is that stablecoins are typically far more centralized than most might expect. Issuer and administrator controls can freeze, pause, and sometimes effectively claw back funds, even when holders think they are holding something “cash-like.” This is not necessarily a bad thing. Though those who see crypto’s dream of self-sovereign finance think so. Typical consumers and product people in finance businesses likely see the value in the controls. I promise I am not here to trash stablecoins! They are one of the best uses for crypto to come along yet. I just believe consumers should understand what they own and how their tools work. And product / businesspeople building workflows around them as well. Looking at how this asset is often described, it at least appears a lot of folks don’t know a lot of the following issues about stablecoins. These are the kinds of things I like to explore.

Consumer and business crypto users should understand there is a quiet structural reality that’s under-discussed outside of more technical or compliance-aware circles. The general crypto meme that often gets sold is that crypto is “self-custody so no one can touch it” and it may feel that way if looking at a balance in your personal wallet. Assuming you use a self-custody wallet and keep your keys safe, this is true for bitcoin, but not necessarily true for issuer-administered ERC-20s tokens. The phrase “custody” can get over-applied. For personal wallets, self-custody really means: you control the private key that can sign transactions. It does not automatically mean: the asset can’t be frozen, transfers can’t be blocked, redemption can’t be denied, or that the rules can’t change via upgrades and admin roles. With bitcoin, controlling the key is basically the whole story. With many stablecoins, controlling the key is only one layer.

Stablecoin Primer & Growth

Stablecoins are crypto tokens designed to hold a relatively stable price, most commonly one U.S. dollar per token. They let people move “dollars” of a sort on blockchains without the volatility of assets like Bitcoin or Ethereum or any other of the thousands of tokens available. The idea is that stablecoins maintain a target a 1:1 value peg to the dollar, meaning 1 token should trade around $1 most of the time.

The market has been elevating this asset because crypto needed a stable unit of account for trading and settlement. (We’ll leave aside any philosophical ironies as to why that’s not bitcoin.) Early approaches to stablecoins included crypto-collateralized designs and “algorithmic” experiments, and then fiat-backed models that promise redeemability for real dollars held in reserves. It’s this last option that seems to have taken hold and for good reason. Over time, stablecoins expanded from an exchange convenience into something closer to modern money plumbing. They’ve become the default quoting currency on many venues, a key building block for DeFi lending and borrowing, and a useful instrument for moving value cross-border at any time of day. (See: The History of Stablecoins, Tether) Another benefit that’s emerging is stablecoins are likely a decent payment method for some agentic uses; that is, agent / bot software that may operate on its own might need to transact at some point. Stablecoins are one of several ways to do that, but likely an easy option to use for some machine to machine, (M2M), transactions.

Here’s a graphic on How are stablecoins minted and redeemed from Chiara Munaretto. If interested in depth on how fiat currency turns to crypto, see my article: How Does Fiat Become Cryptocurrency?

Calling a stablecoin a “Digital dollar” is a fair mental model, but there are some not-so-subtle differences. For starters, you’re holding a token that references a dollar claim, it’s not actually a dollar. Stablecoins are issued by private entities, not governments. It’s a fantastic business if you can manage to be one of the top coins and maintain large reserves. A lot of folks want in, though the reality is the ecosystem only needs a handful of trusted sources. In fact, too many stablecoin issuer wannabes likely just begs for more risk; especially in terms of liquidity for small issuers. The stablecoin industry writ large is, of course, it’s own separate topic. The point is, these are businesses, not governments even if the vibe they try to give off is that level of stability. Anyway, many major stablecoins will still be subject to laws and compliance obligations, and also technical controls to enforce them. By the way, you’ve likely heard of Central Bank Digital Currencies. (CBDCs). If or where a country issues such a thing, this is seen by some as a type of stablecoin, but it’s really not. It’s in its own category because it’s actually sovereign digital money; basically a direct claim or liability of a central bank. This doesn’t necessarily make them stable though. Because the question is always, “stable in relation to what?” That’s really true of any of these things. Typically, they’re pegged to the U.S. Dollar, but they don’t have to be.

That said, this is not just a product design choice. It can become a monetary and geopolitical issue if large numbers of people or businesses in one country start using privately issued dollar stablecoins instead of local currency rails. At that point, the conversation is no longer only about convenience or crypto UX. It starts touching questions of local monetary control, payment system dependence, and who ultimately sits at the policy steering wheel. Consider European concerns about Cryptomercantilism vs. Monetary Sovereignty-Dealing with the Challenge of US Stablecoins for the EU.

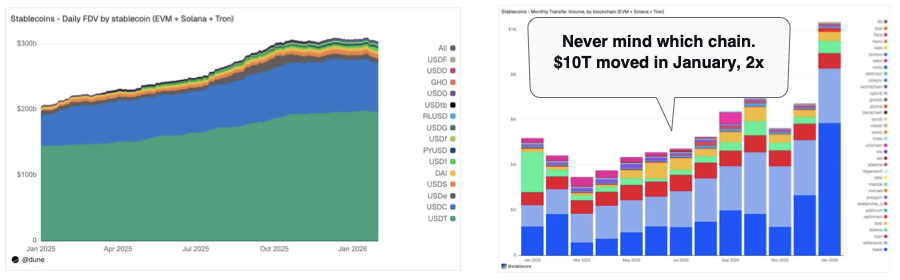

From Dune Blog, ‘Dune Digest 047: Stablecoins Special’…

Beyond the dollar. Non-USD supply remains modest at roughly $1.2B (0.5% of total outstanding), yet 59 local-currency tokens are already live across six continents — nearly 30% of all active stablecoins. Issuers globally are moving quickly to tokenize domestic currencies, often targeting specific payment corridors, remittance flows, or onchain capital markets use cases. […] That shift raises a more important question: what happens when stablecoins stop being primarily dollar-denominated liquidity instruments and start functioning as domestic settlement rails?

This is all is its own very special geopolitical financial system issue we’re not going to get into here beyond this short mention. In any case, just take care with the term “stablecoin”. I’ve been unable to find who first coined it, (pun intended), but it’s brilliant marketing. It’s a very comforting name. Just remember “stable” is a goal. An aspiration. Something that should be maintained. But it’s not necessarily always true. You could theoretically issue a stablecoin and peg it to your commitment to go to the gym more per your New Year’s resolution. Declaring a peg is easy. Maintaining it is the challenge.

From a trust perspective, consumers likely hear “dollar,” and they map it to “cash.” Many stablecoins behave closer to bank money than cash. (“Bank money” means the dollars that exist as ledger entries inside the banking system, not as physical cash. So they’re more like a deposit-like claim.)

Another under-discussed issue, (admittedly just from my perspective), is that not everyone has the same redemption rights. In many cases, large institutions or approved counterparties may be able to redeem directly with an issuer, while ordinary users mostly access stablecoins through exchanges, apps, and secondary markets. That distinction matters. A token can look like a dollar on your screen, but your practical ability to get actual dollars at par may depend on who you are, which platform you use, and what is happening in markets at that moment.

Related to that, people should also ask a boring but important question. If the issuer or a key intermediary fails, what exactly is your legal claim, and to what? The answer can depend on issuer terms, reserve structure, custody arrangements, and jurisdiction. This is one of those topics most people ignore until there is stress. It is also one of the clearest examples of why “digital dollar” is a useful shorthand, but not a full explanation. For anyone who wants to debate this with me, before you do just remember what happened with USDC and SVB in March 2023, TerraUSD in May 2022 (though, ok, that was algorithmic and I’d said this was really about fiat backed), and then Celsius, Voyager, and FTX. True, these last examples were not all stablecoin issuers, but they are exactly the kind of cases that forced people to ask what rights customers actually had in deposited crypto assets during insolvency. And oh yes… Silvergate bank was a good reminder that a lot of “crypto-native” activity still rides on very traditional banking plumbing. When those banks are concentrated and confidence breaks, the stress can spread fast. Let’s not forget issues with Tether, which are supposedly fixed, but we’re talking about problems that are only a handful of years old. (Though here’s a current as of this writing Feb, 2026 article that suggests otherwise Stablecoin giant is crypto’s fragile foundation.) Now… one could argue these were just early failures. People have learned lessons and things are much better now, even just a few years later. Personally, I’d buy that argument. Mostly. I’m still a fan of healthy skepticism though, and diversification and backup plans where appropriate.

Today, stablecoins have quickly come to function as de facto rails in parts of the global crypto economy. You can see that in at least three places, and maybe a fourth:

- Trading and settlement: stablecoins are the base liquidity pair for a huge portion of spot and derivatives activity.

- DeFi: they are the “cash leg” behind borrowing, liquidity pools, and yield strategies.

- Institutional experiments: major payment networks and fintechs have explored stablecoin settlement and integration. (See: Visa Launches Stablecoin Settlement)

- We’re starting to see early usage and infrastructure development for agentic / machine-to-machine transaction use cases.

As of early 2026, public trackers put the stablecoin market in the low $300 billions. (See: Stablecoin market cap hits peak $311.3B) Some expect it to get to the trillions in short order. (See: Stablecoins could drive $1 trillion in T-bill demand.) The key reality check is what sits underneath the stability. If you like, I’d written an older article on how Fiat turns into Crypto.

Source: Dune Blog, ‘Dune Digest 047: Stablecoins Special’ (Feb 21, 2026), Filippo Armani. Visualizations via Dune.

Core Trade-Off: Issuer Kill Switch

Physical cash is hard to control at a distance. Once a twenty dollar bill is in your wallet, nobody can remotely pause it, freeze it, or claw it back. They can only take it by physically seizing it. It may have a serial number, but it’s still considered fungible in that who’s checking serial numbers on bills?

Most major fiat-backed stablecoins are different. They are controlled by so-called smart contracts. These token contracts commonly include administrative powers such as:

- Pausing transfers, sometimes globally.

- Freezing or blacklisting specific addresses.

- In some cases, burning and reissuing tokens in response to a lawful order or a security incident.

When this is done, it’s usually going to be against a particular wallet that’s associated some type of wrongdoing. It’s not about the coin itself. It’s possible that a “tainted” coin could still get seized from an innocent recipient, but this isn’t typically the case. So if a bad guy used illicit proceeds to buy a bag of gummy bears from your online candy store, that stablecoin is still going to be yours. The issuer is not generally going around “clawing back” from downstream recipients just because the payer was shady at some earlier point. However, If the sending address is already on a bad list, you might not be able to receive or use the funds normally. Depending on the token implementation and the wallet/exchange you use, transfers involving a blacklisted address can fail, or you can end up holding funds that are hard to move. “Taint” shows up more at off-ramps than at the token level. Even if the token contract does not mark individual coins, exchanges, payment processors, and banks may use blockchain analytics. If your deposit is linked to a flagged source, they may file reports, etc., freeze your account temporarily, require KYC/proof of source of funds, or actually reject the deposit. This should not the normal outcome for ordinary users, but possible.

These actions are justified as compliance, consumer protection, and incident response. It’s also increasingly consistent with regulatory expectations around sanctions enforcement and anti money laundering. (See: S.1582 – GENIUS Act (now PUBLIC LAW 119–27—JULY 18, 2025) and Markets in Crypto-Assets (MiCA)) If you’re building crypto tools, wallets, exchanges, whatever, we’ve mostly left the wild west. You have to be concerned with various Know Your Customer, (KYC), Anti-Money-Laundering, (AML), global financial crimes block lists and more. Or maybe you don’t. It depends where your business is domiciled, but as a practical matter if you want customers from a variety of countries, you’re going to run into these jurisdictional rules.

None of these controls are automatically sinister. They’re meant to be protective. They can be helpful when funds are stolen or when sanctions must be enforced. But it does change the reality of what people are holding vs. the understanding of many when it comes to the idea of self-sovereign control of crypto assets. You’re likely aware of the different philosophies, but if not, here it is summed up: Crypto purists will lament any ‘outside of self’ control over their assets, (especially government), whereas most typical consumers and businesses mostly couldn’t care less, they just want to go about their day. What is under personal control is what you’re holding and where you hold it. This article is just to help understand more about the nature of this particular asset type.

Issuer Veto In Practice: Freezing At Scale Is Not Hypothetical

These controls aren’t just kind of there in the background. They’ve been used in large ways. Data analyses in late 2025 show Tether and Circle have frozen meaningful amounts over time, with the largest measured in the billions across multi-year windows in some datasets. (See: Tether freezes $3.3B USDT and Circle $109M USDC 2023 to 2025)

Whether you see that as law enforcement cooperation or disturbing financial control, it demonstrates the underlying point. Issuer and administrator roles can immobilize assets at scale, across borders, quickly. Is this great news for catching bad guys? Or Big Brother beyond what even Orwell imagined? You make the call.

Stable is a Target Not a Guarantee

Stablecoins are designed to trade near $1, not promised to stay there in every scenario. When a stabledoin’s market price and a dollar diverge, that’s called de-pegging. Stress reveals where the risk actually lives. Remember, you can say something is worth $1, but what matters is what buyers are actually willing to pay and whether there’s real liquidity, meaning enough buyers when sellers show up. In stress events, if buyers step back or redemptions get uncertain, the market price can move fast.

USDC in March 2023 is a clear example of reserve and banking risk showing up fast. USDC briefly traded materially below $1 after Circle disclosed that part of its reserves were held at Silicon Valley Bank as the bank failed, and markets priced uncertainty about immediate redeemability. The peg ultimately recovered, but the lesson should be clear. Even a regulated, fiat-backed stablecoin can de-peg when reserve custody becomes uncertain. (See: USDC Stablecoin and Crypto Market Go Haywire After Silicon Valley Bank Collapses) Everyone should see the irony in this. The punchline is basically: a “digital dollar” designed to reduce crypto volatility briefly de-pegged because of the same kind of banking-system fragility that crypto sometimes positions itself against. It’s a useful reminder that some stablecoin risk is not ‘crypto risk’ at all. It’s old-fashioned banking and liquidity risk, transmitted instantly onto blockchains. Again, irony.

TerraUSD in May 2022 is the catastrophic example. UST was an “algorithmic” stablecoin that relied on reflexive market incentives rather than robust collateral. It de-pegged and collapsed, wiping out massive value and triggering broader contagion. (See: The collapse of Terra stablecoin UST)

There’s also a subtler form of de-peg risk: collateral contamination. If one widely used stablecoin wobbles and other protocols or products rely on it as collateral, liquidity, or a settlement asset, the stress can propagate quickly. (See: USDC depegs after SVB exposure) Have you even seen videos of a super large and complicated dominos setup with lots of twists, turns and other objects? Remember how they fall and you maybe thinking, “oh, I wasn’t sure just how that part was connected?” Mostly the same thing here only some of the dominos might be our asset values.

If you want to learn more about how this works, see Demystifying Crypto – Tokenomics & Stablecoins.

De-pegs are not rare anomalies. They are how markets price uncertainty about reserves, redemption, liquidity, and reflexive leverage. “Reflexive leverage” in this stablecoin context means a setup where the system’s “stability” depends on market confidence, and that confidence itself is supported by prices that can fall, creating a feedback loop. It’s leverage that creates more leverage when things look good, and unwinds violently when things look bad. In a stressed moment, markets ask: “If everyone rushes for the exit, does this thing still hold $1?” If the answer depends on selling assets into a falling market, or on a mechanism that requires fresh buyers to maintain the peg, the system becomes reflexive.

There’s also a deeper money-quality issue underneath all this. In normal life, people tend to assume one dollar is basically the same as any other dollar. Because they are. That assumption can get weaker in stablecoin markets when confidence could vary by issuer, reserve quality, redemption access, or platform. In other words, the market may start pricing not just “a dollar,” but whose dollar-like token it is and how quickly it can really be turned into cash.

The short answer here for the darker scenarios is that if this kind of stuff is going on, everyone is in for a rough ride and there won’t be many places to hide anyway. In true stress events, correlations rise and liquidity disappears, so hedges inside the same ecosystem can fail. The few places to hide in a real stress event tend to be outside crypto, and even those come with trade-offs. Correlations also tend to rise when markets get messy, so diversification is not a magic shield, but it’s still common sense. I’m not a finance professional and this isn’t advice, just an observation about how these episodes seem to play out.

A Practical Map of Ccentralization: Token-level Veto vs System-level Veto

There are at least two layers of centralization to understand in this context:

- Token contract controls

Does the token itself include pause, freeze, blacklist, or admin burn mechanics? - System and collateral controls

Even if the token has no simple blacklist function, can governance, collateral composition, custodians, or redemption chokepoints effectively create similar outcomes?

Fiat-backed stablecoins commonly have token contract controls because issuers need tools to comply with lawful orders and manage incidents. Some decentralized stablecoins avoid token-level blocklists, but can still inherit meaningful system-level risk through governance and collateral choices.

Two examples of nuance that matter:

- DAI: The DAI token is often described as not having a simple issuer blacklist mechanism like USDC or USDT. However, Maker governance and system architecture can still create forms of control and risk. Historically, DAI’s exposure to centralized collateral has also meant it can inherit some censorship and custody risk indirectly. (See: Maker Protocol documentation)

- Synthetic and yield-linked stablecoins: Many stablecoin and yield-token designs market themselves as “more decentralized,” but still have admin roles, permissioning, or compliance constraints in associated issuance, staking, or redemption flows. Claims like “no admin veto” can be too strong once you account for the full system, not just the base token. (See: Ethena audit report)

Other Functional Stablecoin Issues Worth Understanding

The following is just meant to be a fair risk inventory, not to be paranoid about rare events as this industry matures and has added a lot more controls. Nevertheless, the category does have real failure modes that matter more as adoption grows. And this is not to be disparaging towards stables or crypto; they have their uses. A lot of them. As well, it’s not like traditional banks and currencies haven’t had major issues. The goal here is to just make sure that the fast and easy memes aren’t obscuring some basic issues users of these currencies should understand. This is no different than understanding your bank account, (at least in U.S.), is only insured to a certain amount so maybe you want to spread savings around. Or not. The point is to just understand how things work and be explicit about where you choose to assume risk or sort out backup plans.

- Reserve transparency is often weaker than people assume

Many issuers publish attestations rather than full audits, and reserve composition details can be incomplete or hard for typical users to interpret. Concerns about transparency and reserve composition have repeatedly surfaced in mainstream financial coverage and institutional commentary. (See: S&P downgrades its Tether rating) In other words, there’s still some trust issues that need to exist. This doesn’t mean there’s a problem with reserves. Maybe things are fine. It just might be hard to tell sometimes. - Redemption is not the same as price

A stablecoin can trade near $1 most of the time, but what matters in a stress event is who can redeem, how quickly, under what restrictions, and through which banking rails. Redemption is not the same as price. Stablecoins usually trade near $1 because arbitrage assumes redemptions at par are available and reliable. In stress events, what matters is who can redeem, how fast, under what restrictions, and through which banking rails. If redemption access is constrained or uncertain anywhere in the stack, the market price can slip even if the ‘$1 promise’ still exists on paper. - Banking and custody concentration risk

Even “blockchain money” frequently depends on a small set of banks, custodians, and money-market funds. That creates chokepoints and contagion pathways during crises. (See: Holding Steady: The Rise of Stablecoins) There’s also a broader system angle here as stablecoins scale. If more transaction and treasury activity moves into stablecoins, some funds may shift away from traditional bank deposits and into reserve structures tied to money markets and custodians. That does not automatically mean a problem, but it does mean stablecoins are increasingly connected to the same funding, liquidity, and confidence channels that matter in traditional finance. In other words, this is not fully outside the system. It’s becoming another part of it. Or already is really. That’s kind of the point I suppose. No one with any sense uses bitcoin to buy a Snickers bar at the convenience store. But I should be able to pick any card or wallet on my phone and do so easily enough, even with a stablecoin balance from some account. - Sanctions and illicit finance are a persistent tail risk

Stablecoins are genuinely useful for legitimate cross-border value transfer and they can be attractive for sanctions evasion and shadow payment rails. That tension drives regulatory pressure, which in turn reinforces issuer controls. (See: Sanctioned Russia adopts stablecoin shadow payments) - Yield narratives can hide leverage and counterparty exposure

When you see stablecoin yields that look too smooth or too high, risk is usually hiding in counterparty quality, liquidity mismatch, or reflexive leverage. Terra showed the extreme form, but the broader lesson applies to many “safe yield” pitches. (Once again, See: The collapse of Terra stablecoin UST)

The Non-Sensational Conclusion

Stablecoins are increasingly part of modern financial rails because they make dollars programmable, portable, and usable 24/7, and institutions have begun integrating or piloting stablecoin settlement in the real world. In a lot of ways, I see it as the moment where crypto can say “Hey, look guys! We finally found a really useful thing to do with crypto-like things.” (Okay, maybe Real World Asset (RWA) tokenization is catching up fast.) Even if you never hold a stablecoin directly, you may increasingly be involved in transactions where stablecoins are used in the background for settlement, treasury movement, or cross-border routing, even if the front-end experience still looks like a normal payment..

But the stablecoins that dominate real usage are often not censorship-resistant money. They are closer to regulated digital dollars with administrator controls, sometimes necessary, sometimes reassuring, and sometimes surprising if you came to crypto for self-sovereignty.

The practical takeaway is to just have basic literacy in how this all works and adjust your goals accordingly if necessary.

- If you want maximum price stability and liquidity, you are usually accepting issuer veto and reserve or custody risk.

- If you want maximum resistance to intervention, you are usually accepting more complexity, governance risk, and sometimes weaker peg performance under stress.

- If you’re holding stablecoins for value, everything is probably fine. However, just as you may want to have a couple of different bank or brokerage accounts in case there’s a problem with one of them, you may want to use multiple types of stablecoins to avoid any concentration risk of a problem.

Understanding where the control points are is important for anyone making decisions about assets they’re holding.

See Also:

- Stablecoin Data Summaries (from Dune)

- Stablecoins (AFP – The Association for Financial Professionals)

- Stablecoins: Definition, How They Work, and Types (Investopedia)

- Stablecoins Explained | FULL Guide For Beginners (YouTube)

- From Par to Pressure: Liquidity, Redemptions, and Fire Sales with a Systemic Stablecoin (IMF Working Paper .pdf)

- Stablecoins, an ugly scenario: Stable Coins: Are we minting the next crisis?

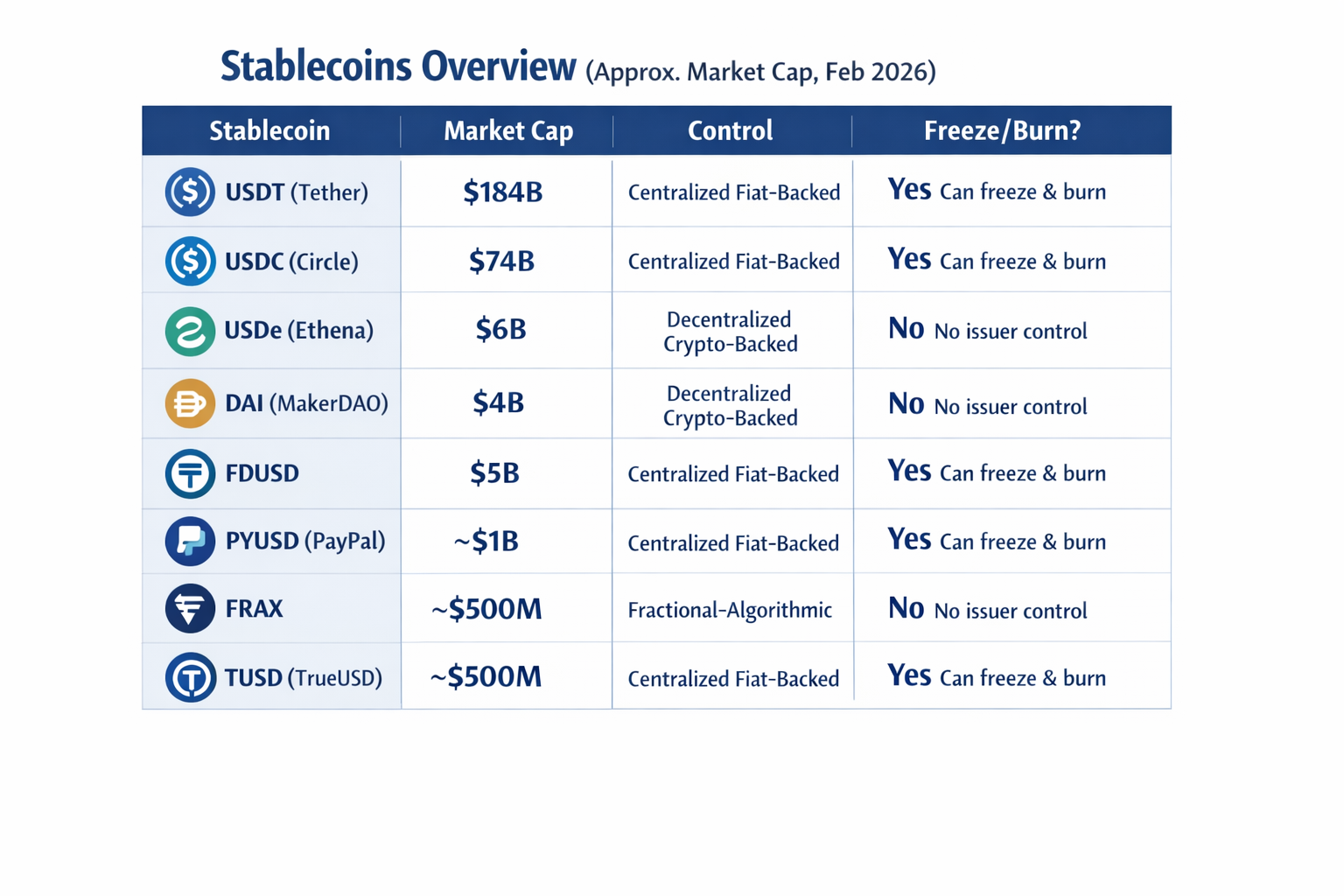

Addendum: Chart of Some Top Stablecoins

THIS IS A SNAPSHOT in time for example only. Things here change fast so if current factual accuracy matters to you regarding anything below, you need to seek out the source and double-check.